Account Aggregator (AA) is a regulated middleman that ensures safe and secure data transfer between Financial Information Providers (banks, mutual funds, insurance companies) and Financial Information Users (individuals, businesses, fintech companies). The user’s data like Bank Account Statements, Income Tax Records, Securities & Investments, Pension Data, Insurance Policies, GST returns, etc are shared in a real-time digitally consented manner for services like loans, wealth management, visa applications, and many more. This data is clean, verified, and encrypted which makes the process of consented data sharing fast, reliable, secure, and democratized.

The digitally consented infrastructure allows users to track their sensitive data and withdraw it at anytime. Users can also choose the duration of data holding with an AA. This, in turn, reduces fraud and speeds up credit access for low-income earners.

What is Account Aggregation?

Account aggregation is the process of collecting and consolidating financial data from multiple bank accounts or financial institutions into a single view. It allows users—or with consent, financial institutions—to access and analyze all their account information (such as savings, loans, credit cards, etc.) in one place. In India, this is facilitated securely through the Account Aggregator (AA) framework, regulated by the RBI, which ensures user consent, data privacy, and controlled access.

How AAs Are Governed

For an entity to operate as an Account Aggregator it needs the approval of the Reserve Bank of India (RBI). They operate under a regulatory framework established by RBI to ensure secure and consent-based sharing of data. AA cannot save or process the information they transmit. They only encrypt the data and transfer it between FIPs and FIUs to ensure safekeeping. RBI periodically audits and inspects AAs for compliance with regulations, and also to check the adequacy of the integrated IT infrastructure and data security. In India, we have Anumati, OneMoney, Finvu, Protean SurakshAA, and many others who are the foundation of India’s digital financial ecosystem—empowering individuals and businesses to seamlessly share bank, tax, and investment data to access credit, insurance, and other financial services.

Regulatory Framework of Account Aggregators (AAs) in India:

- Their classification is NBFC-AAs (a specific type of non-banking organization).

- AAs are not allowed to view, keep, or use user information; they only transmit it securely between the banks and applications that users have faith in.

- Users are always in command: it is their choice on what information to disclose, to whom, and for what duration.

- Every AA uses the same technology to ensure all maintain system uniformity and fluidity.

- The RBI published a framework for identifying Self-Regulatory Organizations for Account Aggregators (SRO-AAs) in March 2025. By maintaining compliance, encouraging best practices, and acting as a point of contact between the industry and regulators, these SROs are meant to supervise the AA ecosystem.

This structure makes it convenient and safer for users to get loans, track finances, and access services — all while keeping their data private and protected.

How Account Aggregators Work?

- User Registers with an AA: The individual signs up with an Account Aggregator and links their financial accounts (like bank accounts, mutual funds, insurance, etc.).

- User Gives Consent: When a financial institution (like a lender) requests access to the user’s financial data, the AA asks the user for explicit, purpose-specific, and time-bound consent.

- AA Collects Data from FIPs: Once the user consents, the AA collects data from Financial Information Providers (FIPs)—such as banks, insurers, or mutual fund platforms—using secure APIs.

- AA Shares Data with FIUs: The AA then securely shares the financial data with the Financial Information Users (FIUs)—like banks or NBFCs—who requested it, and only for the specific duration and purpose approved by the user.

- No Data Storage: Account Aggregators do not store the user’s data. They act as a secure pipeline to transfer encrypted data between FIPs and FIUs.

- Data Sharing is Reversible: Users can revoke consent anytime, stopping the data flow to FIUs.

Everything You Need to Know About AA Apps in India

AA apps act as personal data vaults by giving users dominion over their financial data. To access services like loans, individuals no longer need to go through the outdated, error-prone process of manually sharing documents such as bank statements or tax records. Instead, a faster, more secure, and consent-based ecosystem is now in place. Users can simply download AA apps like Anumati, Finvu, or CAMS Finserv AA, and register by verifying their identity using the mobile number linked to their bank account(s). Once registered, they can link their accounts via net banking or OTP. From there, users are empowered to share specific data with financial institutions — securely, purposefully, and for a limited duration — all with their explicit consent.

AA apps haven’t just simplified data sharing – it’s driving a revolution in data democratization and unification, putting power back in the hands of the user.

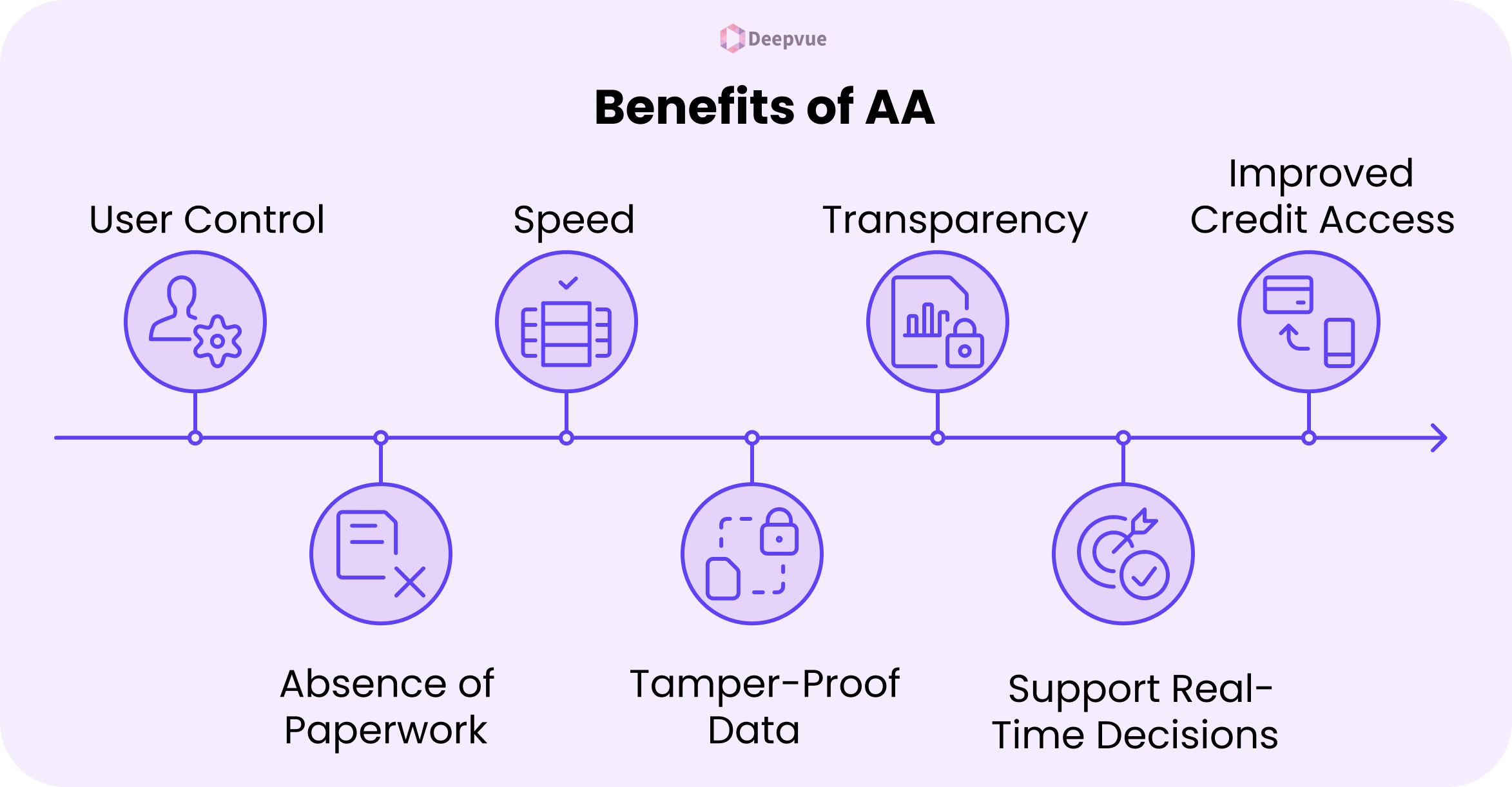

Benefits That’ll Make You Say ‘AA-mazing!’

- User Control: Users can decide how much information to share and for how long.

- Absence of paperwork: Financial documents don’t need to be downloaded, printed, or scanned for sharing across financial institutions.

- Speed: Quicker approvals (for loans, insurance, etc.) result from one-click data transfer. Therefore, loans, insurance, or investments can be processed in minutes, not days.

- Tamper-Proof & Authentic Data: Data shared directly from institutions ensures it’s accurate and can not be manipulated.

- Transparency: Monitor and revoke permissions for data at any time.

- Support Real-Time Decision Making: Financial institutions can make faster, data-backed lending or underwriting decisions.

- Improved Credit Access: Individuals with limited credit history can now use transaction data to access formal credit.

All in all, Account Aggregators are quietly rewriting the rules of finance – one consent, one click, and one empowered user at a time.

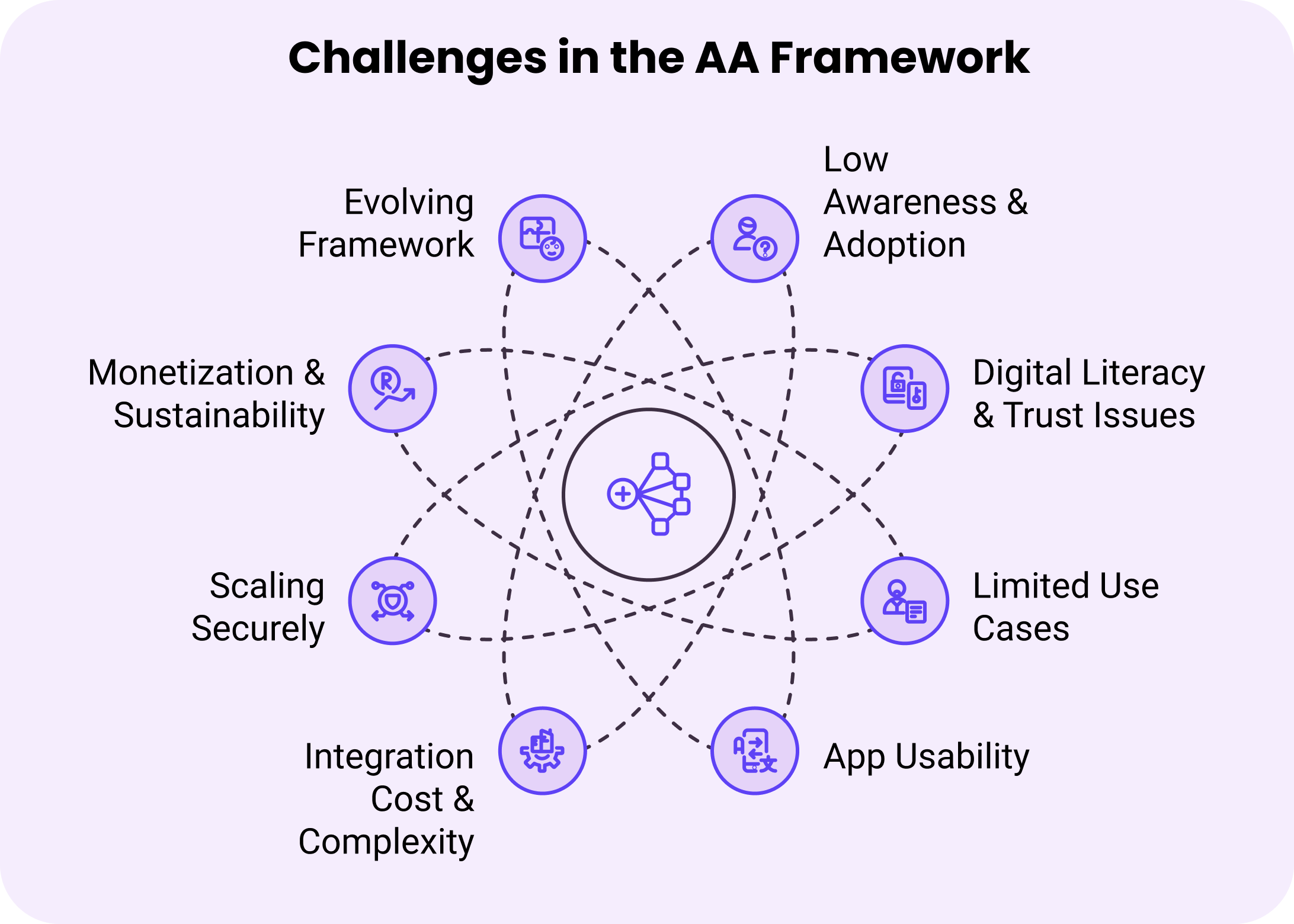

Key Challenges in the AA Framework

While the AA framework is a game-changer, like any other evolving ecosystem, it faces a few shortcomings and blockers. We will see what these shortcomings and blockers are from the perspective of different stakeholders ie., Users, Financial Institutions, AA tech Providers, and Regulatory & Policy Perspectives.

- Low Awareness & Adoption: The majority of people still don’t know what AA is or how it helps them. For the typical user, the idea is intimidating or abstract.

- Digital Literacy & Trust Issues: Even though the process is consent-based, some users are reluctant to share data digitally out of concern about privacy violations or misuse.

- Limited Use Cases (So Far): The advantages are currently more apparent in loan applications. More general everyday applications, like personal finance, tax filing, and insurance, are still in their infancy.

- App Usability: Adoption in rural or semi-urban areas may be restricted by certain AA apps’ continued lack of user-friendly design or multilingual support.

- Integration Cost & Complexity: Being fully operational as Financial Information Providers (FIPs) or Users (FIUs) is still a work in progress for many banks, insurers, and NBFCs. Infrastructure investment and compliance overhead are necessary for the integration with AA tech.

- Scaling Securely: Ensuring strong encryption, uptime, and real-time performance becomes crucial as adoption rises.

- Monetization & Sustainability: The majority of AAs are subject to regulatory price caps. It’s challenging to create a revenue model that is both sustainable and affordable.

- Evolving Framework: The ecosystem of AA is still developing. Careful regulatory calibration is needed for new use cases (such as government data integration, healthcare, or telecom).

The Road Ahead: From Consent to Empowerment

Account Aggregators (AAs) are positioned to become the foundation of personal data ownership as India transitions to a fully digital economy. However, we must change the focus from “data sharing” to “data empowerment” to realize their full potential. This entails making AAs a part of everyday life by extending their use cases beyond loans to include tax filing, investment advice, and financing for education. To make users feel rewarded for properly managing their data, the experience should be fun, easy to use, and maybe even gamified. To facilitate the safe and easy exchange of personal data, AA should be expanded beyond the financial industry to include industries like healthcare, education, and employment.

Above all, providing inclusive access via voice interfaces, lightweight apps, and vernacular support will empower all Indians and establish data ownership as the standard rather than a luxury.