Understanding your credit history is crucial for maintaining financial health and accessing credit opportunities. Whether you’re applying for a loan, a credit card, or even a job, your credit history plays a vital role. In this blog, we will explore what credit history is, why it is important, and how you can manage and improve it.

What is Credit History?

Credit history is a detailed record of your borrowing and repayment activities. It includes information about your loans, credit card usage, payment histories, and any outstanding debts.

This record is maintained by credit bureaus, which collect data from various financial institutions and creditors. Here are the main components of credit history:

Payment History

- This is the record of all your payments on credit accounts, such as credit cards, mortgages, and other loans.

- It includes information about late payments, defaults, and accounts sent to collections.

Credit Utilization

- This represents the ratio of your current credit card balances to your credit limits.

- Lower credit utilization is more favorable as it indicates responsible credit usage.

Age of Credit Accounts

- This refers to the length of your credit history, calculated from the date you opened your oldest account.

- A longer credit history is good as it provides more data on your spending habits and payment behavior.

Credit Mix:

- This is the variety of credit accounts you have, such as credit cards, mortgages, and installment loans.

- A diverse credit mix can positively impact your credit score as it shows you can manage different types of credit.

Inquiries:

- These are recorded when a lender checks your credit history to assess your creditworthiness, usually when you apply for a loan or credit card.

- Multiple inquiries in a short time can negatively affect your credit score.

What is No Credit History?

“No Credit History” refers to a situation where an individual has no record of borrowing or repaying debts, meaning there is no information available for lenders to assess their creditworthiness. This typically occurs when someone has never used credit products such as credit cards, loans, or mortgages, or when their credit activity is too limited to generate a credit report.

Key Points:

- No Credit File: Credit bureaus have no record of the person’s borrowing or repayment history.

- Common Among: Young adults, recent immigrants, or those who have avoided credit products.

- Impact: Lenders may find it difficult to evaluate the risk of lending, potentially leading to higher interest rates or loan denials.

The Role of Credit Bureaus

Credit bureaus, like Equifax, Experian, and TransUnion, collect and maintain credit information. They gather data from various sources, including lenders, creditors, and public records, to create individual credit reports.

- Data Collection: Credit bureaus receive information about your financial behaviors and obligations from lenders and creditors. They also collect public record information, including bankruptcies, tax liens, and court judgments.

- Credit Report Generation: The bureaus compile this information into a credit report, reflecting your credit history. This report includes personal information, account details, inquiries, public records, and a list of companies that have recently accessed your report.

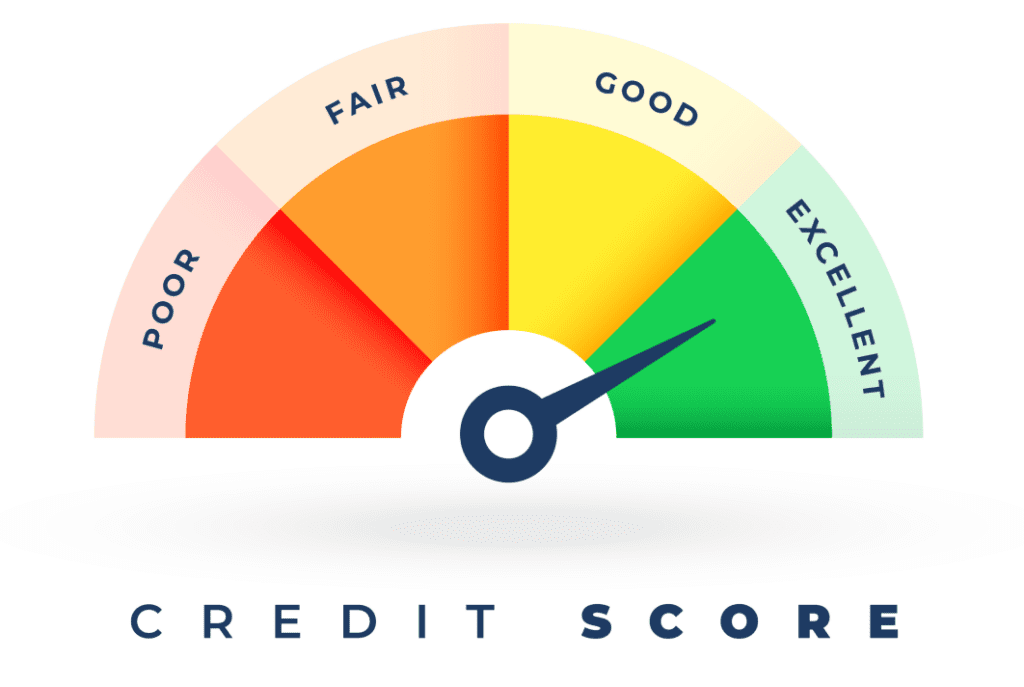

- Credit Score Calculation: Based on the information in your credit report, credit bureaus calculate a credit score. This score is a numerical representation of your creditworthiness, with higher scores indicating lower risk to lenders.

Credit History vs. Credit Score: Key Differences

While credit history and credit score are closely related, they are distinct concepts that play different roles in evaluating creditworthiness:

- Credit History: This is a detailed record of your borrowing and repayment activities over time. It includes information on your credit accounts, payment history, credit utilization, credit age, credit mix, and inquiries. Credit history provides a comprehensive view of your financial behavior and responsibilities.

- Credit Score: This is a numerical representation of your creditworthiness, derived from your credit history. Credit scores are typically calculated using algorithms that consider various aspects of your credit history, such as payment history and credit utilization. The most common credit scoring models are FIC, Experian, TransUnion CIBil, etc. with scores ranging from 300 to 900. Higher scores indicate lower credit risk.

In summary, your credit history is the raw data of your financial behavior, while your credit score is a summary measure of that data, used by lenders to quickly assess your credit risk.

Why is a Credit History Check Important?

A credit history check is a critical determinant in many financial and non-financial decisions. It serves as a risk assessment tool for lenders and impacts various aspects of your financial life.

Impact on Financial Decisions:

- Loan Approvals and Interest Rates: Lenders examine your credit history to decide whether to approve a loan application. A good credit history can lead to loan approval with lower interest rates, while a poor credit history can result in higher rates or rejection.

- Credit Limits: Credit card companies refer to your credit history to set credit limits on new accounts. A positive credit history may result in higher limits, while a negative history could lead to lower limits or denial.

- Insurance Premiums: Some insurance companies use credit information to determine premiums for auto and homeowners insurance. Individuals with poor credit may face higher premiums.

Risk Assessment:

- Risk Evaluation: Lenders use your credit history to evaluate the risk associated with lending money or extending credit to you. It provides insights into your previous financial behaviors, allowing lenders to predict future behaviors.

- Creditworthiness Assessment: Credit history checks help estimate your creditworthiness, determining whether you are likely to meet your financial obligations. This assessment influences the approval, terms, and conditions of loans and credits, affecting your overall borrowing costs.

How to Improve and Maintain a Good Credit History

Maintaining a good credit history is crucial for accessing various financial products and obtaining favorable terms. Here are some strategies:

Building Credit History

- Open a Credit Account: Consider applying for a secured credit card or a small installment loan. Use the credit account responsibly to start building a positive credit history.

- Pay Bills On Time: Regularly pay all your bills, including credit card, utility, and loan payments, before the due date. Set up automatic payments to avoid late payments, which can negatively impact your credit history.

- Maintain Low Credit Utilization: Keep your credit card balances low relative to your credit limits. A lower credit utilization ratio indicates responsible credit management and positively impacts your credit score.

- Avoid Multiple Credit Inquiries: Limit the number of credit applications to avoid multiple inquiries in a short time frame. Too many inquiries can lower your credit score and give the impression of financial instability.

Rectifying Errors in Credit Report

- Review Credit Reports: Obtain your credit report from each of the three major credit bureaus at least once a year. Scrutinize each report for inaccuracies, such as incorrect account statuses, late payments, or debts that aren’t yours.

- Dispute Errors: If you find inaccuracies, file disputes with the respective credit bureaus promptly. Provide any necessary documentation to support your dispute and get the errors rectified.

- Stay Informed: Monitor changes in your credit report regularly to stay informed about your credit status. Use credit monitoring services to receive alerts about significant changes in your credit report.

Consequences of Poor Credit History

A poor credit history can negatively impact your financial well-being. Here’s how –

Difficulty in Obtaining Loans

- Loan Rejections: Lenders may deny loan applications due to a poor credit history reflecting high credit risk. It may be challenging to secure a mortgage, auto loan, or personal loan with unfavorable credit records.

- Higher Interest Rates: If approved for a loan, individuals with poor credit histories may face higher interest rates due to the perceived risk. Higher rates result in increased borrowing costs and financial strain over time.

- Stringent Terms and Conditions: Lenders may impose stricter terms and conditions on loans granted to individuals with poor credit histories. These could include shorter repayment periods, collateral requirements, or co-signer necessities.

Other Implications:

- Rental Applications: Landlords may reject rental applications from individuals with poor credit histories. Those who manage to secure a rental might have to pay higher security deposits.

- Employment Opportunities: Some employers conduct credit checks as part of the hiring process. A poor credit history may hinder employment opportunities, particularly in financial sectors or positions with fiscal responsibilities.

- Insurance Premiums: A poor credit history might result in higher premiums for auto and homeowners insurance. Insurers may perceive individuals with poor credit as high-risk clients, adjusting premiums accordingly.

Conclusion

Credit history is a vital aspect of your financial health. Understanding what it is and why it’s important can help you make informed financial decisions. By maintaining a good credit history, you can secure better financial opportunities and avoid the pitfalls associated with poor credit. Regularly monitor your credit, address any discrepancies, and adopt responsible financial habits to ensure a robust credit history.

To learn more about how Deepvue’s Verification Suite can enhance your online verification process, visit Deepvue.tech and explore their range of APIs designed to ensure accuracy and efficiency.

FAQs

What is a credit history check and how is it conducted?

A credit history check involves reviewing an individual’s credit report, which is compiled by credit bureaus. Lenders, landlords, and employers may conduct these checks to assess creditworthiness and financial responsibility.

How can I get a copy of my credit report?

You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months at AnnualCreditReport.com. You can also request a report if an adverse action has been taken against you based on your credit report.

What factors most significantly impact my credit score?

The most significant factors impacting your credit score are payment history, credit utilization, length of credit history, credit mix, and the number of inquiries. Timely payments and keeping credit card balances low are particularly crucial.

How long do negative items stay on my credit report?

Any remarks/items such as late payments and collections, stay on your credit report for seven years. Bankruptcies can remain for up to 10 years. However, the impact of these remarks reduces over time with responsible financial behavior.

Can I improve my credit score quickly?

Improving your credit score is usually a gradual process. You can boost your score by paying bills on time, reducing outstanding debt, disputing any inaccuracies on your credit report, and avoiding new credit inquiries in a shorter period of time. While there are no quick fixes, consistent responsible behavior will lead to improvements over time.