It has become crucial more than ever to ensure that loans are granted to individuals and businesses who can repay. This process, known as credit underwriting, plays a pivotal role in maintaining the stability of lending institutions.

For companies like Deepvue.tech, which provides API infrastructure for financial integrations and insights, understanding and enhancing the credit underwriting process is vital. This blog will walk you through the credit underwriting process and its importance.

What is Credit Underwriting?

At its core, credit underwriting is the evaluation process that lenders use to assess the risk of lending money to a borrower. It involves analyzing the borrower’s financial history, income, credit score, and other relevant factors to determine whether they are a good candidate for a loan. The primary goal is to minimize the risk of default, ensuring that lenders only extend credit to those who are likely to repay it.

Why is the Credit Underwriting Process Important?

The credit underwriting process serves both lenders and borrowers:

- Protects Lenders: By thoroughly evaluating a borrower’s financial situation, lenders can avoid extending credit to individuals who might struggle to repay, thereby reducing the risk of financial losses.

- Safeguards Borrowers: Borrowers benefit as well, as the process prevents them from taking on more debt than they can handle, promoting financial stability.

- Promotes Financial Inclusion: The credit underwriting process can also take into account non-traditional factors, allowing individuals with limited credit history but strong potential to access credit. This approach fosters financial inclusion by broadening access to loans.

Key Factors in the Credit Underwriting Process

The credit underwriting process involves evaluating several key factors to determine a borrower’s creditworthiness. Here’s a breakdown of the most important ones:

- Credit Score: This three-digit number reflects the borrower’s creditworthiness. It is often the first indicator lenders look at when assessing a borrower’s ability to repay a loan. The higher the credit score, the lower the risk for the lender.

- Credit History: Beyond the credit score, a borrower’s credit history provides a detailed record of their previous loans, credit card usage, and payment patterns. This helps lenders understand the borrower’s behavior when it comes to managing debt.

- Income and Employment Stability: Lenders need to ensure that borrowers have a steady income stream to make their loan payments. By verifying employment history and income through documents like salary slips and tax returns, lenders can assess a borrower’s financial stability.

- Debt-to-Income (DTI) Ratio: This ratio compares a borrower’s total debt to their income. A lower DTI ratio indicates that the borrower has a manageable level of debt relative to their income, making them a lower risk for lenders.

- Collateral: For secured loans, such as a mortgage or auto loan, collateral (like property or a vehicle) is required. Lenders will verify the value and ownership of the collateral to ensure it can be used to recover the loan if the borrower defaults.

How the Credit Underwriting Process Works

Now that we understand the key factors, let’s walk through the credit underwriting process in banks and other financial institutions, particularly in India. This process typically follows a structured sequence of steps:

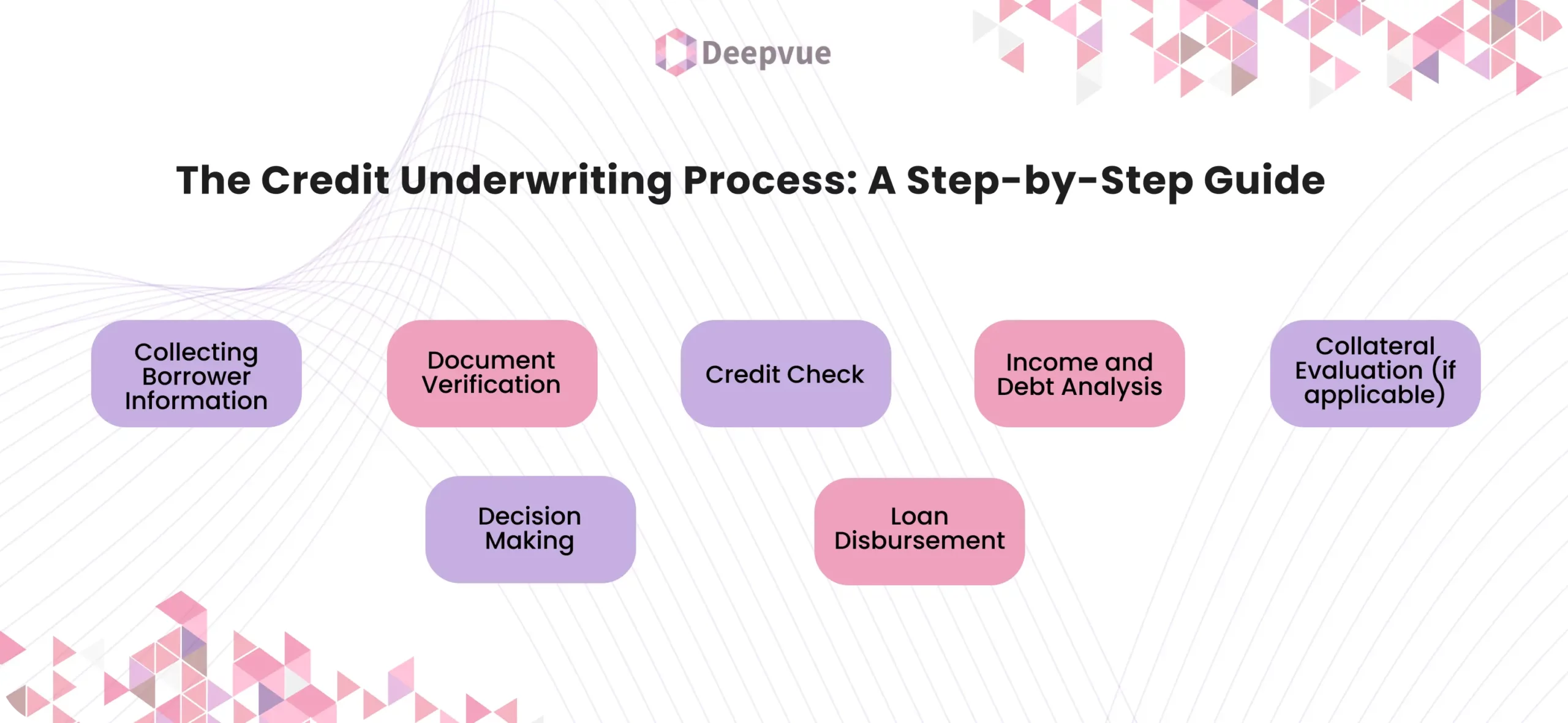

- Collecting Borrower Information: The first step is gathering the necessary information from the borrower. This includes personal details, employment status, income sources, and credit history. Accurate KYC (Know Your Customer) documentation is essential to ensure that the borrower’s identity is verified.

- Document Verification: Next, the lender verifies the documents provided by the borrower. This includes identity proofs, income proofs, and collateral documents (if applicable). Verification ensures that the information is accurate and that the borrower meets the lender’s criteria.

- Credit Check: Lenders will then access the borrower’s credit report from credit bureaus such as CIBIL in India. This report provides a detailed history of the borrower’s past credit behavior, helping the lender identify any potential red flags.

- Income and Debt Analysis: After verifying income and employment details, the lender calculates the borrower’s DTI ratio. This step helps determine whether the borrower has enough income to manage the new loan along with their existing debts.

- Collateral Evaluation (if applicable): For secured loans, the lender will verify the collateral’s value and ownership. This ensures that the collateral is legitimate and sufficient to cover the loan amount if needed.

- Decision-Making: Based on the comprehensive evaluation, the lender makes a decision. The options include loan approval, rejection, or modification of the loan terms. For instance, the lender might offer a lower loan amount or a shorter repayment period to reduce risk.

- Loan Disbursement: If the loan is approved, the lender disburses the funds to the borrower. The borrower then begins making regular payments according to the agreed-upon terms.

Credit Underwriting in India: Special Considerations

The credit underwriting process in India involves some unique factors compared to other regions. For example:

- Use of Aadhaar and PAN for Identity Verification: In India, government-issued documents like Aadhaar and PAN cards are commonly used for verifying a borrower’s identity. This step is crucial to prevent identity fraud and ensure that the correct person is evaluated.

- Role of CIBIL and Other Credit Bureaus: CIBIL (Credit Information Bureau India Limited) plays a significant role in the Indian lending ecosystem. Lenders rely heavily on CIBIL scores and reports to assess a borrower’s creditworthiness.

- Cultural and Economic Factors: India’s diverse economic landscape means that lenders often consider additional factors, such as informal income sources and regional economic conditions, when underwriting loans.

The Role of Automation in the Credit Underwriting Process

Automation is transforming the existing methods used for the credit underwriting process. For companies like Deepvue.tech, which provide API infrastructure for financial integrations, automating parts of the underwriting process can significantly enhance efficiency and accuracy.

- Automated Document Verification: By using advanced algorithms, lenders can automatically verify documents, reducing the time spent on manual checks and minimizing human error.

- Real-Time Credit Scoring: Automated systems can access and analyze a borrower’s credit data in real time, providing instant credit scores and reducing the decision-making time.

- Predictive Analytics: By leveraging data analytics, lenders can predict a borrower’s likelihood of default, allowing for more informed decision-making.

- Scalability: Automation enables lenders to scale their operations without compromising on the accuracy or speed of the underwriting process.

Common Challenges in Credit Underwriting

- Borrowers with little or no credit history make it difficult to assess risk accurately.

- Missing, outdated, or incorrect financial information can lead to incorrect risk assessments.

- Self-employed individuals or those with variable income pose challenges in predicting repayment ability.

- Borrowers with high existing debts may struggle to take on additional credit.

- Inflation, interest rate hikes, or recessions impact borrowers’ repayment capabilities.

- False information in loan applications can lead to inaccurate credit decisions.

- Meeting legal and compliance requirements (e.g., fair lending laws) adds complexity to underwriting.

- Some scoring models may not accurately capture a borrower’s true financial health.

Conclusion

The credit underwriting process is the backbone of responsible lending. By carefully evaluating a borrower’s financial situation, lenders can make informed decisions that protect both themselves and the borrower. For companies like Deepvue.tech, which offer API infrastructure for financial integrations, optimizing this process through automation and technology is key to staying ahead in a competitive market.

In summary, the credit underwriting process involves multiple steps and factors, from collecting borrower information to making the final lending decision. By understanding and streamlining this process, financial institutions can reduce risk, improve efficiency, and promote financial inclusion.

FAQs

What is the purpose of the credit underwriting process?

The credit underwriting process is designed to assess the creditworthiness of potential borrowers. This helps lenders evaluate the risk of lending money and determine whether the borrower can repay the loan. It protects both the lender from financial losses and the borrower from taking on debt they may not be able to manage.

How long does the credit underwriting process typically take?

The duration of the credit underwriting process can vary depending on factors such as the complexity of the borrower’s financial situation, the type of loan, and the efficiency of the lender’s underwriting system. On average, it may take a few days to a couple of weeks to complete.

What documents are required for the credit underwriting process?

Common documents required include government-issued ID (such as PAN or Aadhaar cards), income verification documents (like salary slips, bank statements, or tax returns), credit reports from credit bureaus, and collateral documents (if applicable).

Can I still qualify for a loan if I have a low credit score?

Yes, you may still qualify for a loan with a low credit score, but the terms might be less favorable, such as higher interest rates or stricter repayment conditions. Lenders may also consider additional factors, such as income stability, employment history, and collateral, when making their decision.

How does the credit underwriting process differ in India compared to other countries?

While the core principles of credit underwriting remain similar worldwide, the process in India may place additional emphasis on documents like Aadhaar and PAN cards for identity verification. The role of credit bureaus like CIBIL is also prominent in assessing credit history. Additionally, specific regulations by the Reserve Bank of India (RBI) may influence underwriting practices in Indian banks and financial institutions.