India’s financial market is walking through a complicated terrain characterized by both advancements and new challenges. As the Reserve Bank of India (RBI) records a fall in the gross non-performing assets (GNPA) ratio to a 13-year low of 2.5% as of September 2024, the absolute amount of NPAs has gone up in some parts. For example, in Jharkhand, gross NPAs rose from ₹7,448.78 crore in FY24 to ₹8,194.83 crore in FY25.

These developments highlight the urgent need for aggressive credit monitoring systems. No longer a compliance activity, credit monitoring is now a strategic necessity for financial institutions seeking to manage risks and leverage opportunities for growth.

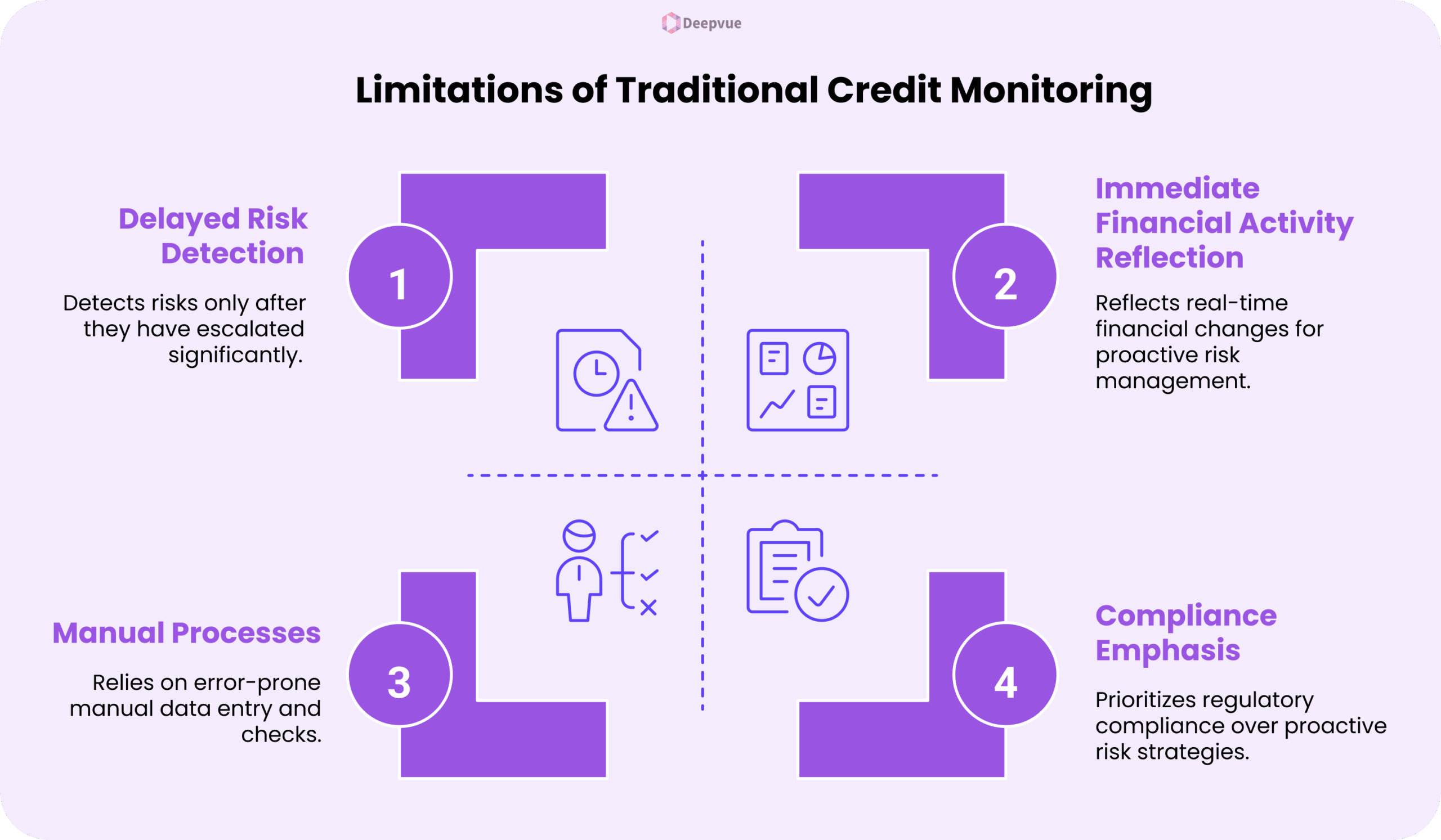

Traditional Credit Monitoring: A Reactive Approach

Credit monitoring entails regular evaluation of borrowers’ creditworthiness, usually quarterly or biannually. This method had a number of weaknesses:

- Delayed Risk Detection: Problems tended to be detected only once they had become serious.

- Manual Processes: Overdependence on spreadsheets and manual checks raised the risk of mistakes.

- Limited Scope: Evaluations were restricted to stagnant data, without reflecting immediate financial activities.

- Compliance-Oriented: The key emphasis was on compliance with regulations instead of proactive risk management.

What Lenders Actually Need Today?

- Real-Time Financial Stress Monitoring: Ongoing surveillance of borrower conduct to observe at an early stage any distress.

- Dynamic FOIR Calculations: Adjusting assessments to present-day income and spending habits.

- Use of Alternate Data for NTC Borrowers: Adding utility bills, purchasing behavior, and other non-traditional data sources.

- Proactive Early Warning Systems: Computerized alerts of potential danger, allowing for early interventions.

- Smart EMI Deduction Mechanisms: NACH presentations tailored to the unique cash cycles of an individual.

How Our Monitoring Stack Powers Proactive Lending: Stress Detection, Early Warnings, and More

To remain competitive, lenders require more than a one-time risk evaluation, they require ongoing, smart visibility into borrower actions. Our credit monitoring solution is intended to close that gap, enabling lenders to identify risk early, respond quickly, and preserve portfolio performance. Here’s how:

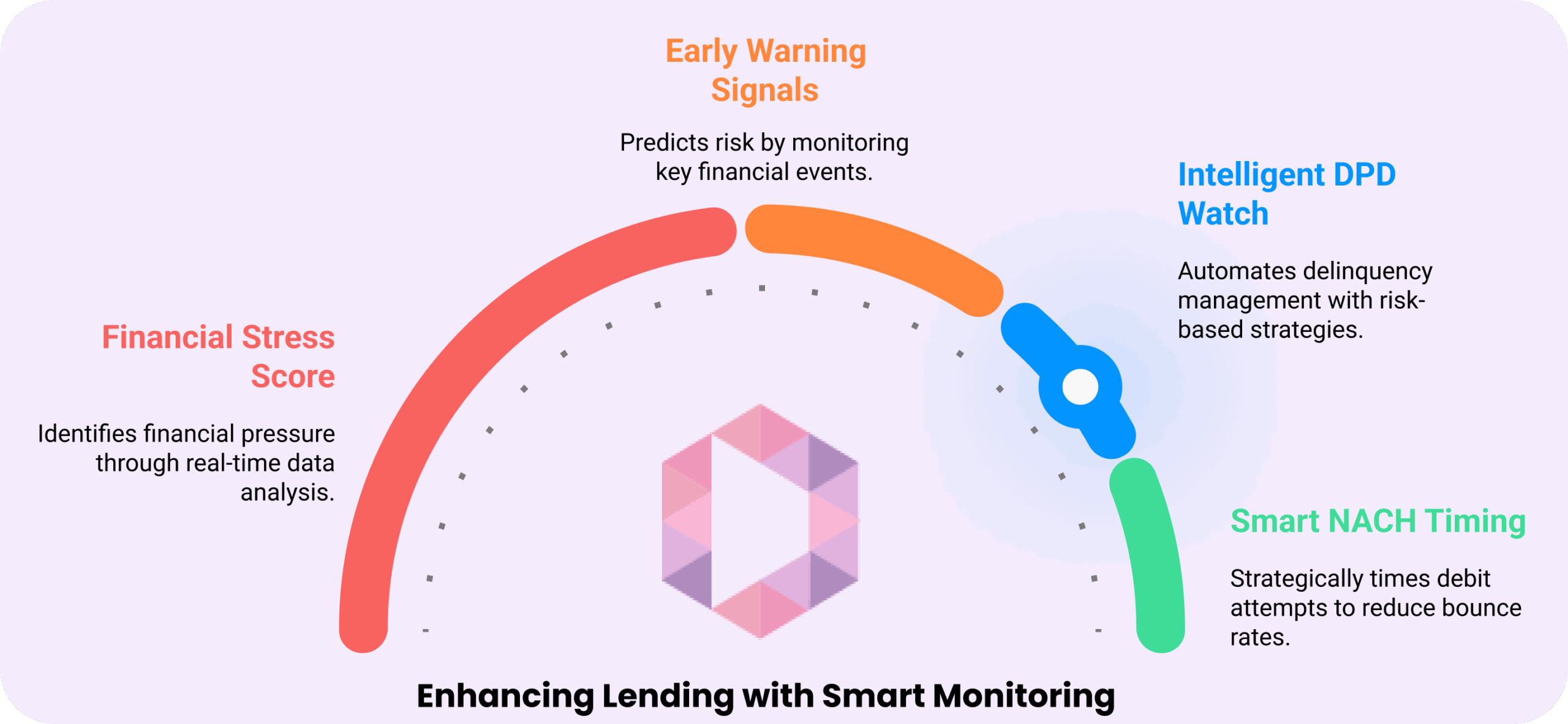

1. Financial Stress Score: Spotting Trouble Before It Strikes

Any defaults tend not to occur overnight but tend to develop over a sequence of increasing financial pressure. Our system combines real-time signals from income streams, spending changes, and payment delays to produce a Financial Stress Score for every borrower. This enables lenders to:

- Prioritize early outreach to at-risk borrowers

- Trigger targeted interventions prior to missed EMIs.

- Decrease delinquencies by intervening in the “pre-default” window.

2. Early Warning Signals Engine: From Reacting to Predicting

Static monitoring has the promise of a default by a borrower. We help lenders shift away from reactive to predictive risk management. Our early warning system continuously searches for events such as:

- Missed salary credits

- Cheque bounces

- Unusual or large withdrawals

- Unexpected spikes or declines in spending

3. Intelligent Days Past Due (DPD) Watch: Smarter, Not Harder

Manually managing delinquencies is time-consuming and frequently unreliable. Our platform monitors DPD status on a borrower basis automatically and initiates:

- Workflow escalations based on aging buckets

- Automated recoveries and recovery prompts

- Prioritized collection strategies based on risk score and DPD stage

4. Smart NACH Presentation Timing & Partial EMI Collection

Most systems default when a borrower’s balance is low on the EMI date. Our platform prevents this by:

- Monitoring check account trends and timing debit attempts strategically (e.g., after salary credit),

- Backs partial EMI allowances, recouping what’s possible without jeopardizing a complete bounce.

The payoff? Reduced bounce rates, enhanced recovery, and healthier borrower relationships.

Why These Features Matter: Real Benefits for Lenders?

- Fewer Defaults and NPAs due to Early Detection

Early warning signals and financial stress scores enable lenders to identify potential difficulties before payments are missed, allowing early interventions that reduce defaults and NPAs. - Enhanced Operational Efficiency through Automation

Automated DPD monitoring and smart NACH scheduling decrease labor, minimize failed EMI collections, and accelerate recovery, making credit management more cost-efficient and streamlined. - Improved Customer Relationships with Customized Repayment Terms

Knowledge of borrower cash flow enables lenders to provide flexible repayment arrangements such as flexible EMI payments and customized schedules, fostering confidence and enhanced retention. - Confident Credit to Thin-File or NTC Borrowers

By applying alternative data like utilities bills and shopping trends, creditworthiness can be determined outside of traditional bureaus in a new segment of borrowers without risk.

Real-World Impact: How Proactive Monitoring Changes Outcomes

- Lower Bounce Rates: Smart EMI deduction timing, coupled with pre-checks, has returned up to 40% fewer failed transactions, lowering penalties and enhancing borrower relationships.

- Declined NPAs: Advance warning signs and financial stress scores enable intervention prior to a borrower missing an EMI, and decline portfolio NPAs by 20-30% in active portfolios.

- Enhanced Recovery Rates: Timely partial EMI collection and real-time DPD monitoring provide timely recoveries that continue uninterrupted and increase recovery rates by up to 15%.

- Improved Risk Pricing and Customer Segmentation: Dynamic FOIR computations and secondary data enable lenders to extend customized interest rates and differentiated credit products, promoting portfolio expansion while managing risk.

Competitive Advantages of Robust Credit Monitoring

- Decrease in Non-Performing Assets: Early identification and action decrease the number of NPAs, maintaining capital and improving profitability.

- Enhanced credit decision-making: Having access to real-time information enables making more precise and quicker credit decisions that enhance business efficiency and customer satisfaction.

- Dynamic Risk-Based Pricing: Advanced risk profiling of individuals enables closer credit product pricing based on individual risk levels, with interest rates calibrated on individual risk.

Embedded Risk Monitoring = Embedded Growth

- More stable cash flows from defaults and delayed payments.

- Real-time dynamic credit transactions that respond to borrower variations in real-time.

- Improved customer satisfaction through active communication and the facility for flexible repayment.

- Competitive differentiation in an increasingly competitive lending market.

Conclusion

Credit monitoring has transformed from a mechanical compliance function to a value-added business function. By adopting best practices in monitoring, financial institutions not only help reduce risks but also open up new avenues of growth and customer interaction. Those institutions that embrace this shift in paradigm shall be more apt to excel in the competitive environment of contemporary finance.

FAQ

What is credit monitoring in the context of lending?

Credit monitoring is the process of monitoring a borrower’s credit history on a real-time or periodic basis in order to gauge credit risk and take preventive action prior to defaults.

Why is real-time credit monitoring important to lenders?

It helps identify early warning signs of financial stress, reduces the possibility of non-performing assets (NPAs), and enables early action, protecting the lender’s portfolio.

How does credit monitoring provide a competitive edge?

It allows lenders to provide custom loan terms, identify risks ahead of time, and react quicker than the competition, enhancing profitability and customer retention.

What technologies enable modern credit monitoring?

Technologies like Account Aggregators (AA), APIs, real-time analytics, and machine learning models empower continuous and automated credit risk assessment.

How does credit monitoring help reduce fraud?

By tracking unusual or suspicious financial behavior as it happens, credit monitoring can flag potential fraud before major financial damage occurs.

![Hand holding an identity card against a purple background with the text "Top 10 PAN Card Verification API Providers In India [2024]" and the Deepvue logo.](https://deepvue.tech/wp-content/uploads/2024/07/Frame-95-scaled.webp)