If running an SME were easy, we would all be sitting on some beach sipping margaritas. We are, instead, juggling budgets and managing people to keep the lights on while trying to scale up. One of the biggest hurdles? Funding. That elusive thing can either accelerate your growth or send you back to square one.

Small and medium enterprises (SMEs) are the backbone of most economies, fueling job creation, innovation, and economic growth. However, most SMEs are still unable to acquire enough funds to grow and expand, or even to sustain themselves for everyday business activities. Therefore, in this blog, we break down the ins and outs of SME lending so that you can navigate the waves and ride your way towards success.

What is SME Lending?

SME lending refers to the finance solutions employed to raise capital for small and medium enterprises. These then match the mobilized capital with the needs of the enterprises. Loans, and lines of credit, among other financial tools tailor-made for SMEs, meet these needs, manage the expenses, fuel growth, and provide a much better operational efficiency in the process. Contrary to traditional business loans, which offer loans for large corporations, SME finance is structured so that its conditions are more flexible and accessible.

Types of SME Loans:

- Term Loans: These loans are paid back over a fixed period as a lump sum. However, most term loans are absorbed for expansion or asset acquisition.

- Working Capital Loans: Short-term loans designed to cover day-to-day funds for operational expenses, including payroll and inventory.

- Invoice Financing: Loans created from outstanding invoices whereby business organizations obtain the cash immediately while waiting for customers to clear their dues.

- Loan for Equipment: Funding especially for the acquisition of equipment purchases or for leasing.

What Lenders Consider When Offering SME Loans?

- Credit Score: A good credit score increases the chances of an SME getting a loan and opting for better terms. Lenders check the business credit history and that of its owners.

- Business Age and Revenue: New companies, especially new start-ups, have problems getting loans since they are still beginning with a no or minimal record of finance. Companies that are relatively older with stable revenue functions have less of a hassle.

- Collateral: Lenders consider the value of collateral when granting secured loans. Businesses without collateral seek unsecured loans or alternative financing.

- Financial Statements and Business Plan: In case, there is a clear financial statement and a sound business plan, then lenders can understand how the loan will be used and how the company will repay it.

Benefits of SME Lending for Business Owners

Access to lending enables SMEs to fund project activities, scale up operations, and respond to market demands. Key benefits include:

- Management of Cash Flow: The SME loans provide working capital through which the regular expenditures of the small business firm may be facilitated to ensure smooth business operations.

- Investment in Growth: Lending allows SMEs to fund expansion plans, such as opening new branches, buying equipment, or expanding product lines.

- Enhanced Credit Profile: Timely loan repayments improve the business’s credit rating, making it easier to access future financing.

- Competitive Edge: With SME credit lending and financial analysis, businesses can better compete in the market, especially when launching new products or investing in technology.

Challenges Faced by SMEs in Securing Loans

- High Rejection Rate: Due to a weak credit rating history or even the lack of some form of collateral that could guarantee lending, most small businesses face higher rejections.

- Lack of Collateral: A lot of SMEs lack essential assets that would be considered for use as collateral and, hence, cannot qualify for a traditional bank loan.

- Regulatory Hurdles: Strict regulatory requirements also throw in regulatory obstacles. This makes the application process for the loan cumbersome and time-consuming.

- Higher Interest Rates for Unsecured Loans: SMEs without collateral often must opt for unsecured loans, which carry higher interest rates, increasing the cost of borrowing.

Tips for SMEs to Improve Their Chances of Loan Approval

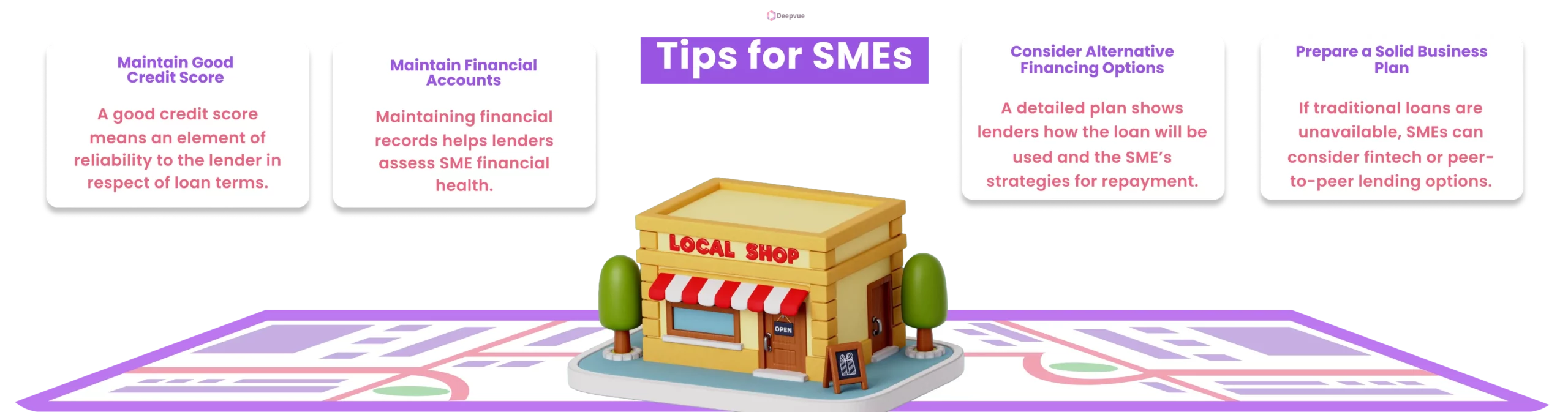

- Maintain Good Credit Score: A good credit score means an element of reliability to the lender in respect of loan terms.

- Maintain Financial Accounts: Maintaining the proper record of financial statements and other associated documents assists the lenders while assessing the financial health of the SME.

- Prepare a Solid Business Plan: A detailed plan shows lenders how the loan will be used and the SME’s strategies for repayment.

- Consider Alternative Financing Options: If traditional loans are hard to obtain, SMEs can explore alternative options, such as fintech or peer-to-peer lending.

The Final Word: SME Lending Made Simple

SME lending can be known as the blood of life, bringing small and medium businesses access to capital for growth, innovation, and sustainability. In a spectrum running from traditional loans to digital and alternative forms of financing, today’s online SME lending has more options than ever. Yet, in such situations, there are stringent lending requirements and a lack of collateral.

If proper preparation and knowledge about what is available are in place, businesses can secure the funding needed to grow into healthy, thriving units and contribute to economic growth development. SMEs’ long-term success prospects shine brightly if proper mechanisms are put in place to overcome financial barriers.

If you’re lending businesses ready to explore your options, reach out to our experts today for personalized advice and guidance to make your lending journey smooth and secure for your customer.

FAQ:

What is SME lending?

SME lending is providing financial products, such as credit and loans, tailored toward the development of small and medium-sized companies to grow their growth while managing expenses.

How is SME lending different from traditional business loans?

Traditional loans are slower, while financing is easier with flexible access, especially when taken from digital or alternative lenders in online SME lending.

What are the eligibility criteria for an SME loan?

The lenders consider business age, revenue, financial history, and whether collateral is offered in addition to credit score.

Can startups get SME loans?

Yes, start-ups can avail of SME loans as well. However, they are prone to high rejection in the process since it is a new business without a financial background and fewer assets.

Are there government programs for SME lending?

Yes, most governments offer a range of programs to assist SMEs, including low-interest loans, grants, and loan guarantees, which make it easier for small businesses to gain access to funding.