Bad debts are not just lost revenue; they can completely dismantle business cash flow, straining operations and limiting growth opportunities. When customers do not pay their dues, losses must be written off by the businesses, and all this causes a trimmed amount of financing sources, a plunge in profitability levels, and an increase in borrowing costs. Unpaid invoices can also have ramifications on relationships with suppliers, resulting in procurement delays, hence disrupting the supply chain.

Preventing bad debts requires proactive risk management, including thorough credit assessments, clear payment terms, and consistent follow-ups. By implementing effective debt prevention strategies, businesses can safeguard their financial health and ensure long-term sustainability.

This blog delves into the true cost of bad debts and offers practical measures to reduce risks and ensure a sound financial standing.

Deciphering Good Debt and Bad Debt

Good debt is borrowing that builds wealth, improves financial security, or raises earning power in the long term. It is likely to have lower interest charges and add up to long-term value.

Examples of Good Debt:

- Student Loans: Investment in education can yield greater earnings and professional development.

- Mortgage Loans: A home can gain equity and appreciation over time.

- Business Loans: Borrowings to expand a business, purchase equipment, or increase productivity will generate more revenues.

- Real Estate Investments: Loans to commercial real estate or investment property are capable of generating passive income.

Bad debt is that debt that never creates future value and tends to carry high interest. The true cost of bad debts is generally funds declining assets or discretionary spending.

Examples of Bad Debt:

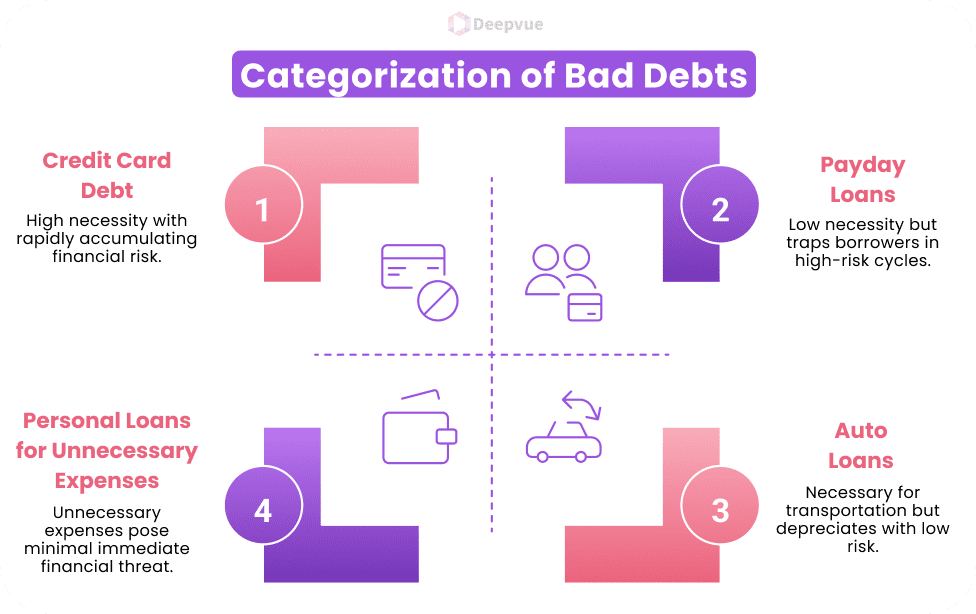

- Credit Card Debt: Quickly accumulating purchases at high interest rates can result in financial distress.

- Payday Loans: Short-term loans with very high interest rates that can lead to a debt cycle.

- Auto Loans: A car loses value over time and is therefore a bad long-term investment.

- Personal Loans for Unnecessary Expenses: Taking a loan for holidays, luxury items, or unnecessary lifestyle enhancements can put one into financial instability

Good debt supports companies to expand, enhance operations, and yield greater returns. Loans for expansion, technology investment, or buying inventory can make a company more profitable. Bad debt is a financial burden to companies as it adds liabilities without revenue. Excessive borrowing or taking high-interest loans may result in cash flow problems and even bankruptcy.

Types of Bad Debts

- Credit Card Debt: Builds up because of high interest charges, late payments, and excessive spending, and thus becomes hard to pay back.

- Uncollectible Receivables: Customer amounts due that are not paid because of financial problems, disputes, or business failures.

- High-Interest Loans: Such as payday loans, personal loans, or subprime lending, in which high interest makes it difficult to repay.

The Financial Impacts of Bad Debt Costs

- Impact on Cash Flow: Real Bad debts reduce the amount of cash received, and thus companies cannot maintain liquidity. This can result in problems in paying the suppliers, employees, and operational costs on time.

- Operational Challenges: If companies encounter bad debt costs, they tend to experience difficulties in allocating funds for development and expansion. Insufficient cash flow could prompt them to reduce investments in new projects or technology.

- Effect on Profit Margins: Bad debt costs have a direct impact on a company’s income, decreasing overall profitability. To offset these losses, companies may have to provision more for doubtful accounts, harming financial statements.

The Ripple Effects of Unpaid Dues

- Damage to Business Reputation: Unpaid dues can harm a company’s credibility and trustworthiness. Investors and suppliers might be reluctant to collaborate with an enterprise that is considered financially unstable.

- Drain of Resources: Companies invest time and money in attempting to collect debts. Legal costs, recovery procedures, and administrative tasks divert resources away from core business.

- Employee Morale and Productivity: Financial instability can result in delayed payments and budget reductions, impacting employees. Staff uncertainty and stress can reduce motivation and job satisfaction.

- Customer Relationships and Trust: Companies can find it challenging to sustain service quality because of financial limitations. Customers can lose faith if a company does not keep promises or takes shortcuts.

- Legal Risks and Consequences: Unpaid debts can lead to lawsuits, fines, or legal action from creditors. Companies can be subject to bankruptcy procedures or asset seizure.

Strategies for Preventing Real Bad Debts

- Credit Risk Assessment: Evaluate the creditworthiness of a customer before extending credit by examining their payment patterns, financial reports, and credit reports.

- Clear Payment Terms and Policies: Establish clear payment terms, including due dates, late charges, and penalties, and inform customers of them before signing contracts.

- Regular Follow-Ups and Communications: Keep customers in regular contact for future payments, outstanding invoices, and past-due balances to minimize defaults.

- Customer Due Diligence: Make comprehensive background checks on customers, confirm their financial standing, and evaluate potential risks before issuing credit or significant transactions.

- Using Payment Plans: Provide customers who are having financial trouble with structured payment plans so that they can pay off their bills without risking full default.

Conclusion

Bad debts can have a serious impact on a business’s financial health, affecting cash flow, profitability, and overall stability. Unpaid dues not only result in loss of revenue but also escalate the cost of doing business, mar creditworthiness, and burden relationships with lenders and suppliers.

One of the best methods to counter the true cost of bad debts is by using real-time financial verification. Our Banking Verification API provides businesses with a powerful solution for the examination of the financial reliability of a customer before any credit can be extended. Get our Banking Verification API today to make better, more data-powered credit decisions, thus protecting your business from unpaid dues

FAQ:

What are bad debts?

Bad debts are unpaid bills or dues that a company cannot possibly get back from its customers or clients. These are generally charged as losses and can be a major drain on a company’s finances.

How do bad debts impact a company’s cash flow?

Bad debts interfere with the cash flow by limiting the funds available for daily operations like supplier payments or growth investments. This, in turn, creates liquidity problems and the inability of the business to meet financial commitments.

How can businesses avoid bad debts?

Bad debts can be avoided by running proper credit checks on customers, establishing clear terms of payment, sending invoices timely, and paying follow-up attention to late accounts.

How do bad debts impact a business’s financial statements?

Bad debts are shown as an expense on the income statement that lowers net profit. On the balance sheet, they lower accounts receivable and total assets, which negatively impacts the company’s financial position.

Which industries are most impacted by bad debts?

Industries with longer credit terms, including construction, manufacturing, wholesale trade, and professional services, tend to be more susceptible to bad debts. Yet any company that offers credit to customers is at risk.