The Unified Payments Interface (UPI) has revolutionized India’s digital transactions, and in 2025, it’s taking another big leap with the launch of UPI-connected credit lines. It is a new feature that allows users to avail pre-approved credit directly within their UPI apps, facilitating the process of borrowing like never before. Rather than just using plain vanilla credit cards or loans, people and companies can now access flexible credit at the moment of payment, on the spot, securely, and with little friction.

In this blog, we demystify what a credit line on UPI is, examine its key benefits, and outline the do’s and don’ts to facilitate safe and beneficial use.

Understanding UPI Credit Line

A UPI Credit Line is a pre-approved digital credit line provided by banks and made available via the Unified Payments Interface (UPI). It enables users to make payments with borrowed money directly from their associated credit line on UPI, like they make payments through a savings or current account on UPI.

How UPI Credit Line Work?

Banks provide a credit limit to such eligible customers that is tied to the UPI ID. Customers can opt to use the credit line as the source of funds while doing a UPI transaction in place of a debit account. The borrowed money is, in turn, repaid according to the repayment terms of the bank, usually with interest-free durations and flexible EMIs.

Benefits of Using UPI Credit Line

- Smooth Digital Payments: Credit line on UPI facilitates payments instantly in real-time through their credit line, just like normal UPI payments, quick, hassle-free, and accepted everywhere.

- Flexibility in Financial Management: Customers are able to control short-term cash flow requirements or emergency expenses without accessing savings, allowing for easier and more flexible financial planning.

- Secure and High-Limit Transactions: Transactions are safeguarded by multi-layer security measures of UPI, and credit lines usually have higher limits compared to regular debit transactions.

- Credit Score Improvements: Careful usage and prompt repayment of the UPI Credit Line can improve the user’s credit record and increase their credit score in the long run.

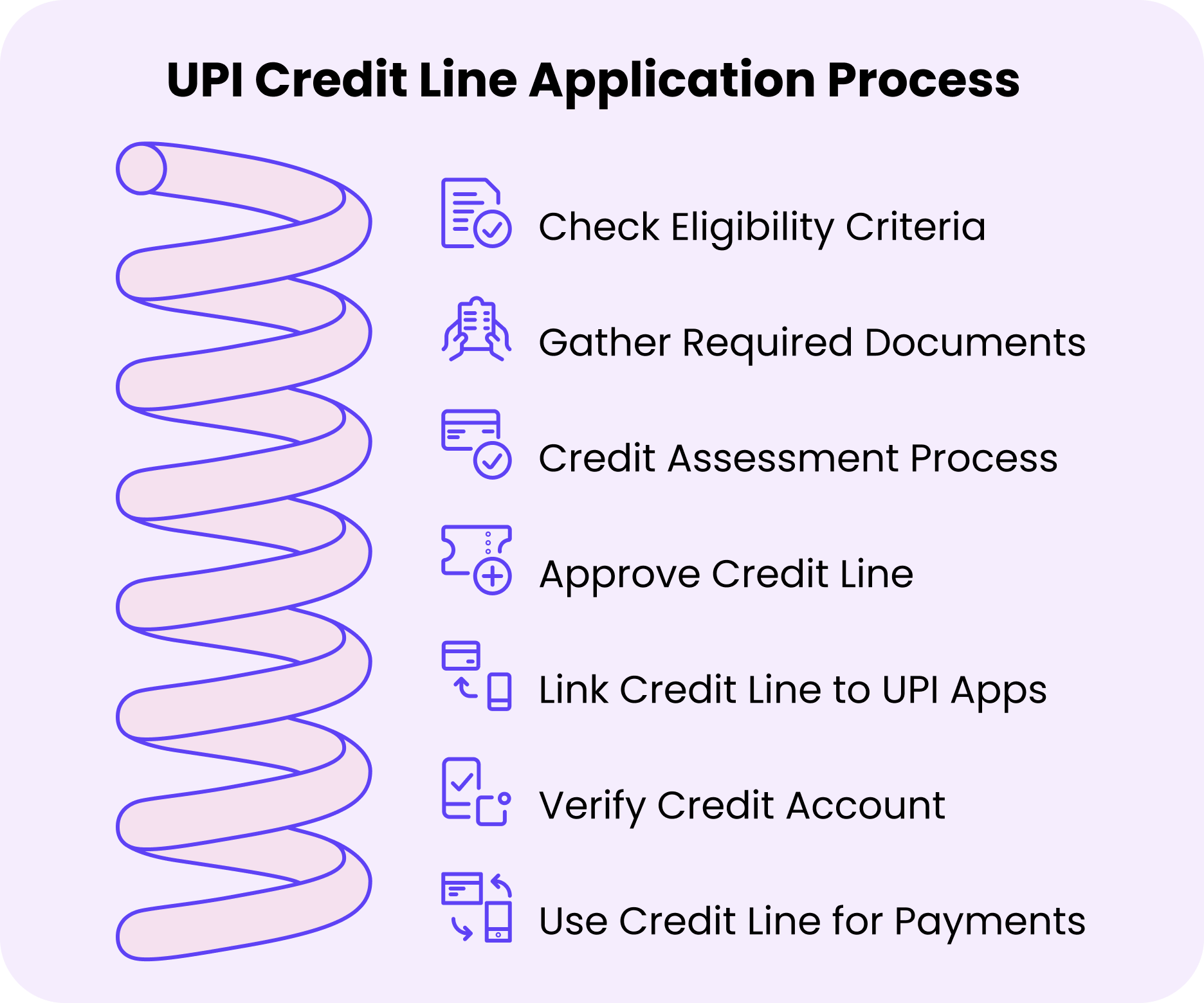

Application Process for UPI Credit Line

Eligibility Criteria

- The candidate should be an Indian resident with a valid mobile number registered against his/her bank account.

- A regular source of income and a sound credit record are typically demanded.

- Candidates should possess a valid PAN and Aadhaar, registered against his/her bank account.

- Age or income-based filters may be employed by some banks or NBFCs.

Documents Required

- PAN Card and Aadhaar Card (for KYC verification purposes)

- Bank statements (typically for the last 3–6 months)

- Income proof, like salary slips or ITR

- Photograph and e-signature, subject to the lender’s onboarding process

Credit Assessment Process

- The lender checks the credit score, stability of income, and repayment behavior of the applicant.

- A soft inquiry can be done through credit bureaus such as CIBIL or Experian.

- A few lenders also employ alternative data, like the pattern of UPI transactions or account aggregators, for underwriting.

- Depending on the risk profile, a credit limit is approved.

Linking Credit Line to UPI Apps

- After approval, the credit line that has been sanctioned is allocated a virtual payment address (VPA) or as a credit account.

- The user can associate this credit line with any UPI-based app such as PhonePe, Google Pay, or BHIM.

- The users will have to verify the credit account through their registered mobile number and UPI PIN.

- Once connected, they may make use of the credit line on UPI for hassle-free UPI payments to vendors or others.

Key Features of UPI Credit Line in 2025

- RuPay Credit Card Integration: UPI has enabled RuPay credit card linking so that users can make payments based on credit directly through UPI apps. This facilitates UPI on credit card transactions with all the UPI-enabled merchants without a POS terminal. It introduces the advantages of credit, like reward points and repayment convenience, into the UPI space.

- Transaction Capabilities: UPI credit line consumers can undertake smooth digital payments through a pre-approved credit limit provided by banks. Payments can be made using UPI QR codes, UPI IDs, or mobile numbers, just like standard UPI transactions. The credit usage is tracked separately from the user’s savings or current account.

- Merchant and Peer-to-Peer Payments: Users can pay both merchants (for shopping, dining, etc.) and individuals using the credit line on UPI. Peer-to-peer (P2P) payments using the credit line are facilitated, providing the liberty to send money even without a real-time bank balance. This makes the UPI credit line a convenient instrument for daily outgoings, both personal and business.

Do’s and Don’ts When Using UPI Credit Line

Essential Do’s

- Only use the credit line on UPI for legitimate and prepaid expenses.

- Maintain a proper track of your transactions both through your UPI app and bank statements.

- Pay your dues in time to save interest, charges, or a credit score effect.

- Set transaction limits to prevent overspending and accidental large transactions.

- Enable app lock and device security to stop unwanted access.

- Notify your bank at once of suspicious or unauthorized transactions.

- Carefully read and understand the terms and conditions of your UPI credit line provider.

- Connect your credit line solely with reliable and verified UPI apps.

Critical Don’ts

- Don’t share your UPI PIN or OTP with anyone, even if they claim to be from the bank.

- Don’t use the credit line on UPI for gambling, speculative investments, or illegal purchases.

- Don’t overlook payment reminders or miss due dates.

- Don’t open untrusted links or read unknown QR codes.

- Don’t link your credit line on UPI unnecessarily to too many apps.

- Don’t use public Wi-Fi to transact, so as not to compromise on data.

- Don’t postpone reporting loss of phone or misuse of your UPI account.

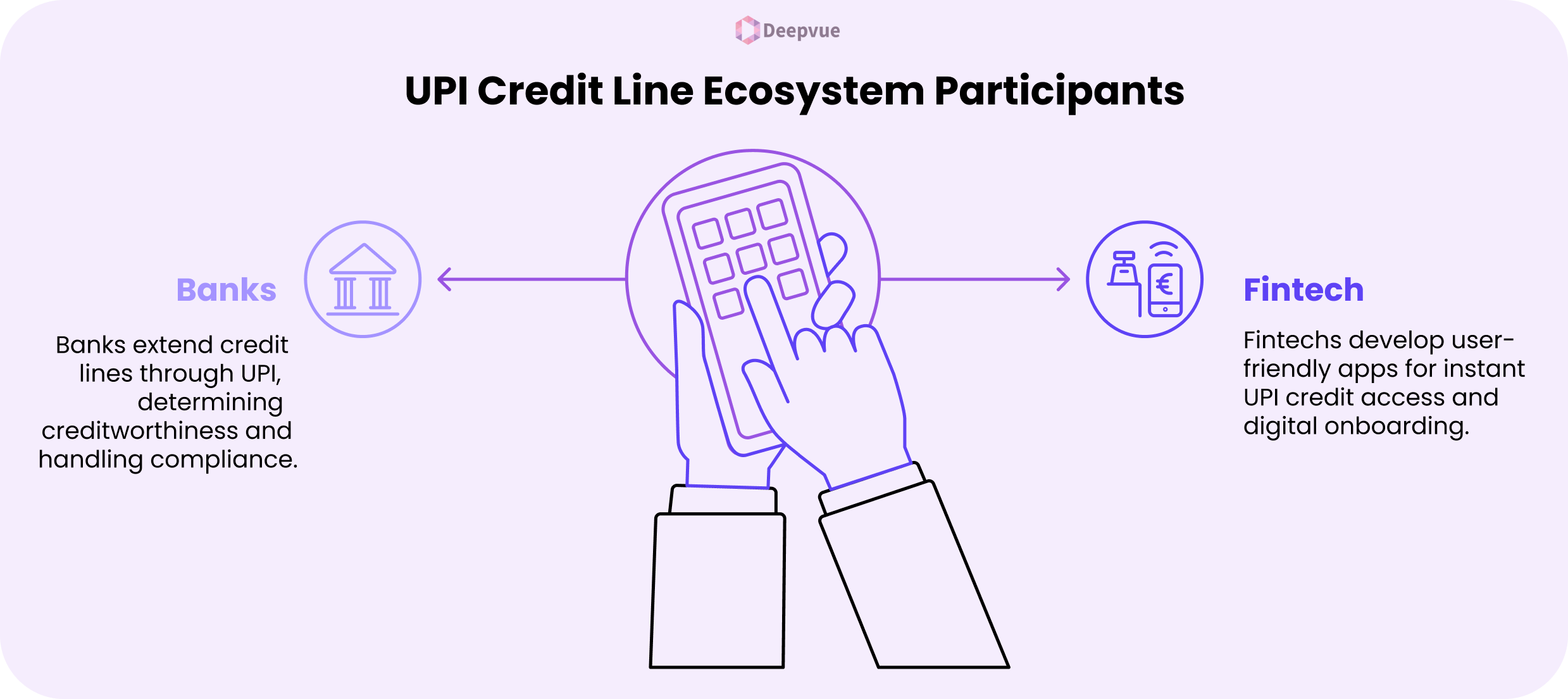

Role of Banks and Fintech in UPI Credit Line Ecosystem

- Financial Assistance by Banks: Regulated and approved credit lines are extended by banks to customers through the UPI platform. They connect with NPCI’s systems to make real-time disbursal and repayment a seamless process. Banks determine creditworthiness and credit limits based on risk profiles and regulatory standards. Banks offer backend infrastructure for account linking, Know Your Customer (KYC) authentication, and compliance.

- Fintech Innovations: Fintechs develop easy-to-use apps through which customers can avail of UPI-based credit immediately. Fintechs make use of alternate data (such as spending habits, mobile consumption, and mobile usage) for instant credit decision-making. Fintechs facilitate hassle-free onboarding through digital KYC and rapid eligibility checks. Fintechs bring instant credit limits, EMI conversion, and payment reminders to the table.

Closing Thoughts

The UPI credit line is an important step in India’s digital financial system, providing users with unprecedented access to instant and hassle-free credit. By combining the convenience of UPI transactions with the versatility of short-term loans, this product empowers individuals and businesses to better manage their finances. However, with any financial tools, prudent use must be followed. Keeping abreast of the terms, repayment schedules, and possible hazards will enable you to get the best out of this facility without draining your finances.

If you’re a fintech, lender, or platform interested in adding UPI credit lines to your products, we can assist you with that. Get in touch with us here to see how our solutions can help enable your business objectives.

FAQ

Can I use UPI with a credit card?

Yes, UPI now supports linking credit cards—primarily RuPay credit cards—for making payments through supported UPI apps.

Are there any additional fees for UPI via a credit card?

While most low-value transactions are free, some merchant payments through credit card on UPI may charge MDR (Merchant Discount Rate), as per the bank and app.

Is a RuPay credit card on UPI free up to ₹2000?

Yes, transactions worth up to ₹2,000 via RuPay credit card through UPI are generally free of extra cost for the customer as well as merchants.

Does Google Pay support Credit Cards?

Yes, Google Pay supports RuPay credit card linking for UPI payments if the card and issuing bank are eligible.