The phrase “dirty money” might conjure images of shady deals and hidden agendas. But what exactly does it mean when these illicit funds get a veneer of legitimacy? This is where the term ‘money laundering’ becomes pivotal. Understanding its mechanics and implications is crucial in today’s global economy. AML or Anti-Money Laundering, policies are the bulwark against the insidious effects of criminal financial maneuvers. They are not just regulatory requirements; they serve as a fortress protecting the integrity of the financial system, thwarting the financing of terrorism, and disrupting the flow of funds from drug trafficking and other illegal activities. Approaching a complex subject, this article unwraps the fabric of AML, detailing its importance, functionality, and ramifications across various industries. It also dive into the severe consequences of non-compliance and outlines the steps involved in establishing a robust AML program. Stay tuned as we navigate the intricate world of anti-money laundering measures and their evolving landscape.

What is Money Laundering?

Money laundering is the illicit process of making large amounts of money generated by a criminal activity, such as drug trafficking or terrorism financing, appear to be earned legitimately. It is a complex method that criminals use to disguise the original ownership and control of the proceeds of criminal conduct by making such proceeds appear to have derived from a legitimate source. The money from the criminal activity is considered dirty, and the process “launders” it to make it look clean.

The process of money laundering can be broken down into three main stages:

- Placement: Illicit funds are introduced into the financial system.

- Layering: Complex series of transactions are conducted to confuse the audit trail and sever the link with the original crime.

- Integration: The now “clean” money is reintegrated into the economy, and appears to come from a legitimate source, which may include investments into businesses, real estate, or luxury assets.

Controls to prevent money laundering include:

- Know Your Customer (KYC) checks

- Software filtering to flag unusual patterns

- Holding periods for large deposits

These controls help in the detection and prevention of suspicious activities related to money laundering, aiding regulatory agencies in combating this financial crime.

What is Anti-Money Laundering?

Anti-Money Laundering (AML) is a crucial set of policies, procedures, and technologies that are put in place to prevent money laundering. It involves monitoring financial transactions and activities to detect and report any suspicious or fraudulent behavior that could potentially be involved in hiding illegal funds. AML regulations are implemented within government systems and large financial institutions to ensure compliance with laws and regulations aimed at combating money laundering activities.

The Importance of Anti-Money Laundering (AML)

Anti-Money Laundering (AML) measures are vital components in the global financial sector that serve as the front line of defense against the infiltration and abuse of financial systems by criminals and terrorists. AML frameworks are designed to detect and disrupt financial transactions related to criminal activity such as drug trafficking, terrorist financing, illegal arms sales, fraud, and many other financial crimes, which pose serious threats to international security and the stability of financial markets.

The implementation of AML controls hinders the ability of criminals to process their “dirty money.” With robust AML strategies in place, it becomes exceedingly challenging for illicit earnings to traverse the financial system undetected. This not only enhances the overall safety within the financial environment but also contributes to the broader fight against the financing of harmful activities.

Compliance with AML laws and regulations is critical for businesses, particularly in the financial sector, as it wards off reputational and operational risks. Inadequate AML protections can lead to severe financial consequences, including crippling fines and penalties. Furthermore, institutions and their employees could face serious legal actions, highlighting the gravity of adhering to these requirements.

Beyond the immediate financial impact, AML laws play an instrumental role in combating tax evasion and other related illegal activities. Banks and other financial institutions are on the frontline of this battle, tasked with the ongoing monitoring of financial transactions and the obligation to report suspicious activities. These measures help in maintaining not only the integrity of individual institutions but also that of the financial system as a whole.

Protecting the Financial System

AML efforts are integral to maintaining the integrity and stability of the financial system. Financial institutions are mandated to establish comprehensive AML compliance programs that include policies, procedures, and controls tailored to their specific risk profiles. These programs are intended to facilitate the ongoing monitoring of customer behaviour and the scrutiny of financial transactions to identify potentially suspicious activities that may indicate money laundering.

The integration of “clean” money into the financial system has the potential to corrupt legitimate economic activities and inflate asset prices, such as in the real estate market. Active enforcement of AML regulations, therefore, provides a necessary barrier against such outcomes. Moreover, advancements in technology, such as biometric identification, have strengthened these efforts, aligning operational procedures with stringent international AML standards.

Non-compliance with these regulatory frameworks can result in far-reaching consequences, including monetary penalties and irreversible damage to the reputations of financial institutions. The operational burden and the increased cost of compliance due to enhanced scrutiny and required remediation efforts underscore the significance of AML regulations as a cornerstone of a secure and reliable financial sector.

Preventing Terrorism Financing

AML initiatives are equally crucial in the domain of national and global security, playing a pivotal role in preventing the financing of terrorist activities. Institutions such as the European Commission perform rigorous risk assessments to detect and mitigate vulnerabilities specific to the EU’s internal market that could be exploited for money laundering and terrorist financing.

The traceability of financial transactions acts as a strong deterrent to such nefarious activities. Over the years, the EU has enacted robust AML directives, starting with the first anti-money laundering Directive in 1990, to combat these dual threats effectively. These legislative measures require financial institutions to maintain thorough documentation of their risk assessments and due diligence processes, ensuring transparency and accountability in compliance with regulatory demands.

AML risk assessments empower financial organizations to pinpoint weaknesses within their systems, allocate resources judiciously, and develop targeted strategies to thwart the financing of terrorism. By identifying potential risks, these institutions can actively take preventative steps to safeguard against the exploitation of the financial sector for nefarious purposes.

Combating Drug Trafficking and Other Illegal Activities

The battle against drug trafficking and a host of other illicit activities is significantly bolstered through AML measures. Profits from drug sales often necessitate laundering to appear legitimate, and traffickers employ tactics such as bulk cash smuggling, the strategic placement of structured deposits, and using money service businesses to conceal the origins of these funds.

Dark web marketplaces facilitate a shadow economy where illicit drug transactions occur, and within these platforms, money laundering techniques are employed to hide the identities of those involved and to protect their ill-gotten gains from detection and seizure. For instance, in the cryptocurrency realm, tumblers are used as mixing services that shuffle currencies to obfuscate the source, blurring the trail back to the illegal activities.

AML measures are directed at disrupting the financial infrastructure that supports such criminal enterprises. By implementing AML regulations, incentives for a range of illegal activities including terrorism financing, corruption, and fraud are greatly diminished. This not only protects the integrity of financial systems but also contributes to a broader societal benefit by reducing the prevalence of criminal activity.

History of Anti-Money Laundering (AML)

The history of Anti-Money Laundering (AML) dates back to the 1970s, when the United States introduced the Bank Secrecy Act (BSA) to combat the growing use of illicit funds in drug trafficking and organized crime. In 1989, the G7 nations established the Financial Action Task Force (FATF) to set global AML standards, leading to the development of the FATF’s 40 Recommendations in the 1990s.

After the 9/11 attacks, AML regulations expanded to include counter-terrorism financing, with laws like the USA PATRIOT Act increasing surveillance and reporting requirements. Over time, international bodies like the UN, IMF, and World Bank pushed for stronger AML frameworks. In recent years, AML has evolved with technology, using AI, transaction monitoring, and digital identity tools to detect financial crimes.

Key Components of AML

Anti-Money Laundering initiatives hinge on several key components, each designed to address the multifaceted nature of financial crimes. Emerging next-generation AML strategies are enhancing traditional approaches by incorporating advanced technologies. These technologies, such as artificial intelligence (AI) and machine learning, provide a significant boost in the effectiveness of detection, prevention, and enforcement actions associated with combating money laundering activities.

AI and machine machine learning algorithms play a pivotal role by scrutinizing vast datasets to discern intricate patterns that signify money laundering, thereby increasing accuracy and reducing the rate of false positives that often burden financial institutions. Moreover, big data analytics platforms serve to amalgamate and analyze information from a multitude of sources, granting deeper insights into potential money laundering risks and facilitating a broader, more informed approach to AML operations.

Another innovative tool in the AML arsenal is blockchain analysis. By allowing investigators to trace and evaluate transactions within blockchain networks, these tools greatly increase transparency and traceability of funds, which are essential qualities in AML efforts.

The key components of next-generation AML involve leveraging these groundbreaking approaches and technologies, which, collectively, improve the precision of transaction monitoring and boost the identification of suspicious financial activities.

Know Your Customer (KYC)

The process of Know Your Customer (KYC) stands as a critical element in the anti-money laundering framework, serving as the first line of defense in the financial sector’s effort to thwart illicit financial flows. KYC is designed to verify the identity of customers and the legitimacy of their capital – a fundamental step to prevent money laundering from the moment an individual or entity seeks to establish a financial relationship or deposit money.

As part of the broader AML spectrum, financial institutions rely heavily on KYC procedures to counteract and identify possible criminal activities like money laundering and the financing of terrorism. During the KYC process, financial institutions gather essential information about their customers, confirm their identities, and continuously monitor ongoing transactions to ensure that these do not partake in financial crimes or raise red flags indicative of illegal undertakings.

Customer Due Diligence (CDD)

Customer Due Diligence (CDD) is integral to Anti-Money Laundering regulations and is mandated for financial institutions to carry out in their ongoing fight against money laundering and terrorist financing. The key aim of CDD is to obtain comprehensive knowledge about customers and their financial behaviors, enabling the timely identification of irregularities that could suggest illicit activities.

Financial institutions are required to enforce CDD measures in various situations, such as when a client commences a new relationship, carries out transactions above certain thresholds, or engages in activities that might be construed as related to money laundering or terrorist financing. To comply with AML regulations, robust CDD protocols must be developed, incorporating transaction monitoring systems to detect and report any dubious financial transactions.

The goal of such painstaking diligence is twofold: maintaining extensive records that detail the nature of customer relationships and transactional flows, and ensuring pertinent information is accessible to law enforcement agencies when necessary, thus reinforcing the global initiative to combat financial crimes.

Suspicious Activity Monitoring and Reporting

Advancements in technology, including artificial intelligence, are being increasingly leveraged in the realm of AML to automate the surveillance of suspicious activities, thereby enhancing the identification and interception of complex financial crimes. SAS financial crimes solutions, for example, employ sophisticated analytical techniques including neural networks, deep learning, and unsupervised learning to unearth previously undetected schemes and progressively adapt to the evasive tactics utilized in the realm of financial misconduct.

A prime feature facilitated by these technologies is intelligent alert prioritization, which channels investigative efforts by highlighting the most pertinent alerts for further scrutiny while minimizing attention to less significant ones. Adding to this capability is the alert/case enrichment functionality, which provides AML investigators with a wealth of relevant information such as previous cases, SARs, third-party data, maps, and transaction histories, greatly enriching the investigative process.

Furthermore, the automation of Suspicious Activity Report (SAR) filing is executed through natural language generation and processing tools, transforming complex data arrays into coherent and readable narratives. This acceleration and streamlining of the SAR filing process not only expedites compliance activities but also amplifies the overall effectiveness of regulatory compliance efforts in the financial sector.

What Is the Difference Between AML, CDD, and KYC?

AML is the overarching framework to combat financial crime.

KYC is the process of verifying identity as part of AML compliance.

CDD is the risk assessment and monitoring aspect within KYC.

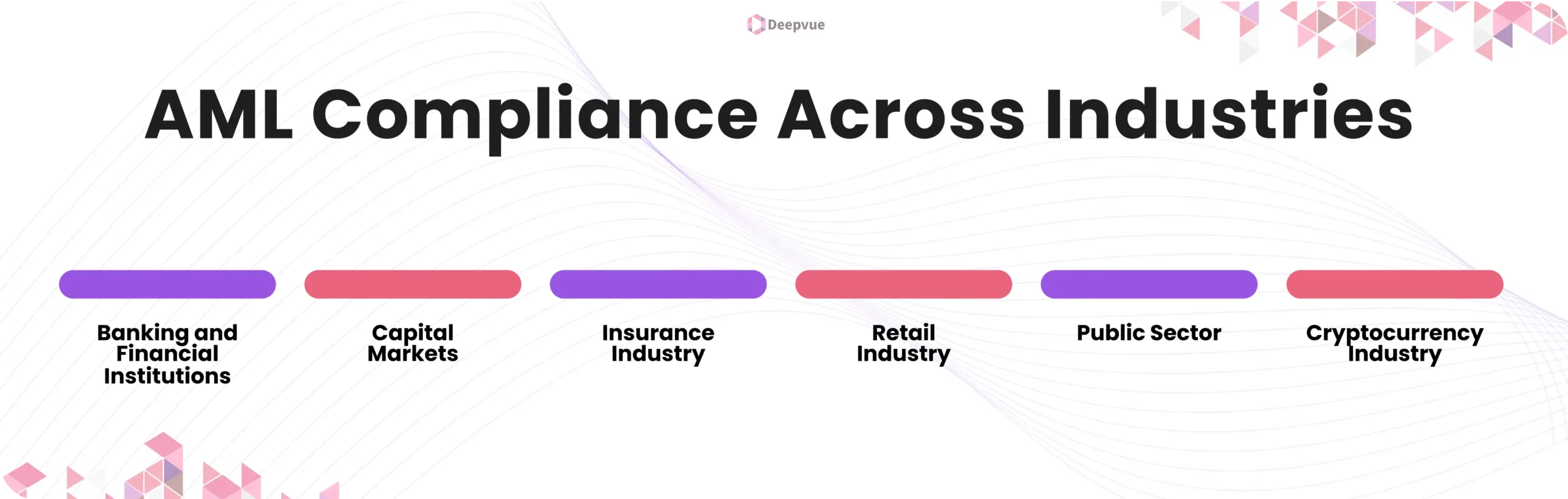

AML Compliance Across Industries

Anti-Money Laundering (AML) compliance is a critical component across various industries, not just limited to the financial sector. Regulatory frameworks such as the USA PATRIOT Act, the Bank Secrecy Act (BSA), and international standards set by the Financial Action Task Force (FATF) mandate companies to establish robust measures to detect and prevent financial crimes. Failure to observe these regulations can result in significant fines and reputational damage.

Modern AML compliance solutions help automate the monitoring and reporting processes, thus enhancing efficiency and reducing errors. These technologies often integrate core features like Customer Due Diligence (CDD) and transaction monitoring systems to flag and investigate suspicious activities. In the U.S., policies under BSA compel banks to create effective AML compliance programs that include customer due diligence systems and procedures for reporting suspicious activities.

Banking and Financial Institutions

Banks and financial institutions form the backbone of the global economy and, as such, are attractive targets for the integration of illicit funds. To combat the potential for unwitting involvement in criminal activities such as drug trafficking and terrorism financing, these institutions must adhere to rigorous AML practices. This adherence is overseen by entities like the Financial Crimes Enforcement Network (FinCEN) and international organizations, which mandate documentation and continuous training as part of AML compliance. Banking operations employ a detailed process of AML and Know Your Customer (KYC), involving customer identification and risk assessments to comply with regulatory requirements and safeguard the financial system.

Capital Markets

In capital markets, firms employ AML solutions to detect and report on fraudulent and illicit activities efficiently. By reducing exposure to fraud and financial crimes, such marketplaces benefit from heightened security. Investment firms leverage technology to facilitate the detection and reporting of suspicious transactions and irregular activities that can compromise financial security. Capital markets firms, therefore, apply ALT technology to improve fraud detection capabilities, comply with regulatory requirements, and manage associated costs.

Insurance Industry

Insurance companies must abide by AML regulations—which include supervising customer activities and reporting suspicious transactions—to deter money laundering and adhere to national and international compliance standards. Financial Investigative Units (FIUs) receive and investigate Suspicious Activity Reports (SARs) from the insurance sector. It is essential for these companies to establish stringent internal controls to prevent penalties and damage to their reputation. Furthermore, insurance entities are tasked with customer verification processes that are integral to AML practices.

Retail Industry

Retail businesses are traditionally seen as low-risk for money laundering, primarily due to the smaller amounts of cash they handle. Yet, they still need to implement AML controls such as Customer Due Diligence (CDD) to prevent usage of shell companies for illicit activities and adhere to financial regulations. While the retail industry may be associated with a comparatively low volume of financial transactions, the sector takes preventative measures against money laundering risks inherent in any commercial transactions.

Public Sector

The public sector, though not typically regarded as a high-risk environment for money laundering, has still experienced incidents involving government officials engaging in laundering activities. In response, initiatives such as beneficial ownership disclosure and anti-corruption legislation have been introduced to mitigate this risk. Accusations against government officials emphasize the need for consistent diligence in implementing and enforcing measures designed to combat money laundering within the public sphere.

Anti-Money Laundering in Cryptocurrency

Given their decentralized and pseudonymous nature, cryptocurrencies are under considerable regulatory scrutiny. As regulatory bodies craft tailored AML frameworks for digital currencies, cryptocurrency businesses are compelled to establish reliable AML policies to build trust and meet regulatory requirements. Exchanges within the industry are enhancing AML practices through KYC requirements and sophisticated technologies for transaction monitoring. Collaboration among various stakeholders, including regulators and law enforcement, is pivotal in developing and maintaining compliance in the rapidly evolving cryptocurrency market.

Key AML Measures in Cryptocurrency:

- KYC and Customer Due Diligence (CDD): Exchanges and wallet providers are required to verify user identities.

- Transaction Monitoring: Analyzing blockchain transactions to identify patterns indicative of money laundering.

- Travel Rule Compliance: Sharing sender and recipient information for cryptocurrency transfers above a specific threshold.

- Blockchain Analytics: Leveraging advanced tools to trace transactions on public blockchains.

Penalties and Risks of Ignoring AML Regulations

Financial institutions that neglect their obligations under Anti-Money Laundering regulations face a chain reaction of severe consequences with far-reaching implications. The consequences of non-compliance are not only punitive in nature, such as fines and penalties but also extend to reputational damage which can erode the trust and confidence of customers and partners alike. Additionally, institutions often confront the risk of losing valuable business opportunities, and in the most grievous circumstances, financial institutions and their employees may face criminal charges. To maintain integrity within the financial sector, adherence to AML laws is a paramount duty of these institutions, and failure to comply can carry substantial regulatory and legal repercussions.

Fines and Penalties

Since 2008, regulators around the globe have imposed fines exceeding $403 billion for violations of KYC and AML mandates. These steep monetary penalties underscore the seriousness with which international and national regulatory bodies tackle non-compliance. The cost inflicted upon banking institutions for failing to comply can vastly exceed the expenses associated with establishing and maintaining comprehensive AML programs. Regulatory agencies, including the likes of FinCEN, actively oversee compliance and do not hesitate to penalize violations, which can also lead to the revocation of business licenses. Such punitive measures act as a potent deterrent and a reminder of the significant benefits that a robust AML framework offers, beyond just avoiding fines, in enhancing a bank’s reputation and trustworthiness.

Reputational Damage

The consequence of a tarnished reputation is a dire one for any financial institution implicated in money laundering activities. Reputational damage results from unfavorable publicity which can shake the confidence that clients place in the institution’s integrity, leaving a lasting impact that often proves more challenging to rectify than financial penalties. To shield themselves against such risks, organizations have increasingly adopted strict KYC and Know Your Employee (KYE) procedures. These measures not only prevent illicit activities but also serve as countermeasures against potential reputational harm, emphasizing the value of a reputation as an intangible yet essential asset.

Loss of Business Opportunities

In the context of the financial industry, loss of reputation can have a cascading effect on business opportunities. Scandals and negative associations can lead to customer discouragement and attrition, which in turn impacts the financial institution’s ability to attract new business. Moreover, ongoing AML investigations and the rigor of maintaining compliance can disrupt normal business functions, resulting in inefficiencies. Additionally, resources that could be channeled towards business growth are often reallocated to deal with the compliance burdens, thereby further limiting opportunities for expansion and innovation in service offerings.

Criminal Charges

The gravest outcome of AML regulation non-compliance is the potential for criminal charges against the financial institution and its employees. AML laws necessitate vigilant monitoring of transactions to prevent the facilitation of money laundering activities. The multi-faceted nature of money laundering, consisting of the stages of placement, layering, and integration, makes it a complex crime that is difficult to trace and dismantle. Financial institutions, therefore, bear the responsibility to act in accordance with the Bank Secrecy Act, as administered by FinCEN, to prevent their services from being used for illicit purposes like money laundering and terrorist financing. Non-compliance is met with stringent enforcement actions and can lead to the levelling of criminal charges, which can have a crippling effect on the institution’s operational capabilities and long-term viability.

International Anti-Money Laundering (AML)

Money laundering is a global concern as criminals and terrorists use complex financial systems to disguise illicit funds. International Anti-Money Laundering (AML) regulations aim to combat these activities by promoting transparency and accountability in financial operations across borders.

Key Components of International AML Regulations:

- Financial Action Task Force (FATF): An intergovernmental body that sets global AML standards and evaluates countries’ compliance.

- Know Your Customer (KYC) Requirements: Ensures businesses verify the identities of their customers to prevent fraudulent activities.

- Suspicious Activity Reporting (SAR): Mandates financial institutions to report unusual or suspicious transactions.

- Cross-Border Cooperation: Nations collaborate by sharing intelligence and implementing unified financial crime prevention measures.

Global AML Regulations and Regulatory Authorities by Country

1. United States

- Regulations: Bank Secrecy Act (BSA), USA PATRIOT Act

- Regulatory Authorities:

- Financial Crimes Enforcement Network (FinCEN)

- Office of the Comptroller of the Currency (OCC)

- Federal Reserve

- Securities and Exchange Commission (SEC)

2. United Kingdom

- Regulations: Money Laundering, Terrorist Financing and Transfer of Funds Regulations (MLRs) 2017 (amended)

- Regulatory Authorities:

- Financial Conduct Authority (FCA)

- Her Majesty’s Revenue and Customs (HMRC)

- National Crime Agency (NCA)

3. European Union

- Regulations: EU AML Directives (6AMLD currently in force)

- Regulatory Authorities:

- European Banking Authority (EBA)

- National financial intelligence units (e.g., Tracfin in France, FIU-Net coordination)

4. Australia

- Regulations: Anti-Money Laundering and Counter-Terrorism Financing Act 2006

- Regulatory Authority: Australian Transaction Reports and Analysis Centre (AUSTRAC)

5. India

- Regulations: Prevention of Money Laundering Act (PMLA), 2002

- Regulatory Authorities:

- Financial Intelligence Unit – India (FIU-IND)

- Reserve Bank of India (RBI)

- Securities and Exchange Board of India (SEBI)

Implementing an AML Program

Implementing an effective Anti-Money Laundering (AML) program is critical for financial institutions and other entities susceptible to financial crimes. This program encompasses a comprehensive set of measures designed to prevent, detect, and report potential money laundering or terrorist financing activities. To ensure rigorous compliance with AML standards, businesses are required to adhere to a multifaceted strategy, which includes five key pillars:

- Appointing an AML Compliance Officer: A designated individual responsible for overseeing the AML compliance program and ensuring its effectiveness.

- Creating Internal Policies and Procedures: Customized frameworks tailored to the organization’s risk exposure, defining how to identify, manage, and mitigate money laundering risks.

- Continuous AML Training: Regular training for employees to stay abreast of AML regulations and understand their role in enforcing them.

- Independent Testing: Engaging third-party auditors to assess the robustness and compliance of the AML program.

- Customer Due Diligence (CDD): In-depth verification of customer identities, risk profiles, and the nature of their financial activities.

A crucial aspect of an AML program is the integration of stringent Know Your Customer (KYC) protocols, which bolster traceability and scrutiny of financial transactions. Cutting-edge technologies such as Machine Learning are increasingly utilized to enhance the accuracy and efficiency of monitoring systems, thus enabling the real-time detection of suspicious activities.

Overall, a robust AML program is instrumental in reinforcing the financial industry’s defenses against illicit activities, while also aligning with global regulatory standards and safeguarding the institution’s reputation.

Establishing AML Policies and Procedures

For any financial institution to stand firm against money laundering, it must first establish robust AML policies and procedures. These measures should be meticulously designed to reflect the organization’s unique risk profile and the requirements laid out by regulatory bodies. Key components of AML policies typically include:

- Strategies for conducting thorough customer due diligence (CDD).

- Processes for ongoing monitoring of transactions to detect anomalies.

- Protocols for reporting suspicious activities effectively and confidentially.

Instituting sound identity verification measures is at the heart of implementing strong KYC and CDD practices. Moreover, when dealing with high-risk customers or large transactions, enhanced due diligence (EDD) becomes a necessity. To manage this, financial institutions often deploy sophisticated, automated transaction monitoring systems capable of sifting through data to flag potential red flags of money laundering or illicit activities.

Conducting AML Risk Assessments

Periodic AML risk assessments are indispensable in identifying and evaluating an institution’s risk exposures. These assessments guide the strategies and specific controls that should be put in place to mitigate identified vulnerabilities. Maintaining meticulous records of these assessments, including the methodologies and findings, is not merely a best practice but also a regulatory necessity, helping demonstrate compliance during inspections by regulatory agencies.

Risk assessments are ongoing processes and serve as a core element of an overarching AML compliance program. Given their critical nature, they must accurately inform the development of internal AML control mechanisms, thereby enhancing the institution’s ability to preempt and preclude potential money laundering activities.

Training Employees on AML Procedures

To further reinforce an AML framework, ongoing employee training is essential. These sessions should inform staff across all functions about the importance of AML compliance, the regulations that govern it, and the specific role employees play in detecting and reporting suspicious activity. Such training encourages a vigilant and proactive stance among employees, fostering an enterprise-wide culture of compliance.

Records of these training sessions are pivotal, ensuring that all team members are consistently aligned with evolving AML regulations. Additionally, these records serve as evidence of the institution’s commitment to regulatory compliance. By educating employees about the procedures for reporting suspicious transactions, financial institutions bolster their front-line defenses against money laundering.

Conducting Regular Audits and Reviews

To validate the effectiveness and compliance of AML programs, regular audits and reviews are a necessity. These assessments can be conducted internally or by external auditors and are geared towards ensuring ongoing adherence to AML-related regulatory requirements.

Audits should be frequent enough to keep pace with regulatory developments and organizational changes. They not only highlight areas open to enhancement but also demonstrate the institution’s dedication to maintaining a stringent compliance program. Regular reviews of ALS procedures reaffirm the institution’s status in the fight against money laundering, serving as a testament to upholding international standards of regulatory compliance.

Staying Updated with AML Regulations

In the rapidly evolving landscape of financial transactions and compliance, staying current with Anti-Money Laundering (AML) regulations is critical for institutions operating within the financial sector. Entities are tasked with proactive tracking of legislative developments and regulatory updates, often prescribed by various international and national regulatory agencies. Adapting AML policies and procedures in light of new information ensures that organizations not only adhere to legal requirements but also bolster their defenses against the ever-changing tactics deployed in money laundering and terrorist financing.

Moreover, AIL regulations in the United States have expanded significantly since the Bank Secrecy Act of 1970, which introduced the reporting requirement for cash deposits exceeding $10,000 and mandated the maintenance of comprehensive transaction records. It is imperative for financial institutions within the U.S. to effectively detect and report suspicious transactions through Suspicious Activity Reports (SARs) to the relevant financial agencies. Such reports are critical tools for law enforcement agencies in their investigations into illicit financial activities.

Regular compliance reviews and audits serve as cornerstones of a sound AML program, uncovering areas that necessitate improvement and validating the effectiveness of existing processes and controls. Additionally, engagement with regulatory authorities and law enforcement agencies enhances the collaborative effort needed to tackle financial crime effectively.

Monitoring Regulatory Changes

Constant vigilance for changes in AML laws and standards is a necessary practice for financial entities. Monitoring regulatory changes empowers organizations to adjust their policies and controls in compliance with new AML requirements. This process is crucial not only for legal adherence but also for aligning with international best practices in preventing the proliferation of financial crimes.

Maintaining a close relationship with regulatory bodies ensures that financial institutions are privy to the latest intelligence and regulatory expectations. Ongoing training for staff members on updated AML regulations, detection techniques, and reporting obligations is integral to cultivating an informed workforce that can actively participate in the detection and prevention of money laundering and terrorism financing.

Engaging in Industry Associations

Engagement with industry associations plays a valuable role in staying at the forefront of AML knowledge and practices. Organizations such as the Association of Certified Anti-Money Laundering Specialists (ACAMS) provide resources, networking opportunities, and certifications that are pivotal for career advancement within the AML field. The Certified Anti-Money Laundering Specialist (CAMS) certification, offered by associations like ACAMS, is recognized internationally and reinforces an individual’s expertise in AML regulations and practices.

Public sector AML specialists find diverse career paths open to them, ranging from policy writing and legal consultation to active roles in law enforcement agencies.

AML careers span across various departments, including information technology, finance, compliance, research, and investigation, demonstrating the interdisciplinary nature of fighting financial crime. Engaging in industry associations keeps professionals abreast of AML trends, reinforces their commitment to regulatory compliance, and equips them with the tools needed for effective AML operations.

FAQs about AML

What is anti-money laundering (AML)?

Anti-Money Laundering (AML) refers to the set of laws, regulations, and measures that financial institutions and other entities must adhere to in order to detect, prevent, and combat money laundering, terrorist financing, and other financial crimes.

Why is AML important?

AML is important because money laundering allows criminals to disguise illicit funds as legitimate, making it difficult to trace their origins and disrupt criminal activities. By implementing AML measures, governments and financial institutions can protect their financial systems, maintain integrity, and contribute to the global fight against organized crime and terrorism.

How does AML work?

AML works through a combination of policies, procedures, and controls that financial institutions put in place to identify and monitor potentially suspicious activities, conduct due diligence on customers and transactions, report suspicious transactions to the authorities, and comply with regulatory requirements.

Who is responsible for enforcing AML laws?

AML laws are primarily enforced by regulatory and supervisory authorities, such as financial intelligence units, central banks, and government agencies. These entities are responsible for overseeing compliance, conducting investigations, imposing penalties, and cooperating with international counterparts in combating money laundering.

What are some common AML measures used by financial institutions?

Common AML measures include customer due diligence (CDD), enhanced due diligence (EDD) for high-risk customers, transaction monitoring, suspicious activity reporting (SAR), staff training and education, and implementing AML software and technologies for automated detection and analysis.

Are all financial institutions required to have AML programs?

Yes, most jurisdictions around the world require financial institutions, including banks, credit unions, securities firms, insurance companies, money services businesses, and casinos, to establish and maintain robust AML programs.

What are the consequences of non-compliance with AML laws?

Non-compliance with AML laws can result in severe consequences, including fines, penalties, loss of licenses, reputational damage, and legal actions. In some cases, individuals involved in money laundering can face criminal charges and imprisonment.

What is the role of technology in AML?

Technology plays a significant role in AML by enabling financial institutions to enhance their detection capabilities, automate monitoring processes, analyze large volumes of data for suspicious patterns, and strengthen their overall AML programs. Advanced technologies like artificial intelligence and machine learning are increasingly used to enhance AML effectiveness.

How can individuals contribute to AML efforts?

Individuals can contribute to AML efforts by being vigilant and reporting any suspicious activities or transactions to the appropriate authorities or their financial institution. It is important to stay informed about AML regulations and best practices and to cooperate with institutions in providing necessary information during customer due diligence processes.

Is AML a global initiative?

Yes, AML is a global initiative. Countries around the world have enacted AML laws and regulations, and there are international organizations, such as the Financial Action Task Force (FATF), that provide guidance and facilitate cooperation among nations in combating money laundering and terrorist financing.