Ensuring the safety and integrity of banking operations is extremely important in the current times. One of the most critical components of this is the Know Your Customer (KYC) process. So, what is KYC in banking, and why is it important? Let’s dive into the details to understand this crucial process and its significance.

What is KYC in Banking?

KYC, or Know Your Customer, is a process that banks and financial institutions use to verify the identity of their customers. This means making sure that the person opening an account or conducting transactions is who they say they are. The main goal of KYC is to prevent illegal activities like money laundering, fraud, and financing of terrorism.

KYC typically happens when you open a new account with any financial service provider, but it doesn’t stop there. Banks, financial institutes, fintechs, continue to monitor and verify their customers’ identities over time to keep everything secure.

Documents for KYC

- Proof of identity (POI) documents are necessary to verify your identity. These include Aadhaar Card, PAN Card, Passport, Voter ID, or Driving License.

- Address proof (POA) documents confirm your current residential address. These may include Aadhaar Card, Passport, utility bills (like electricity, water, or gas), recent bank account statements, or property tax receipts.

- Banks may also require recent passport-sized photographs for record-keeping.

- For non-resident Indians (NRIs), additional documents such as a passport, proof of overseas address, and work or residence visa are required.

- For businesses, banks typically ask for the company PAN Card, certificate of incorporation, MoA and AoA, address proof, and KYC documents of the authorized signatories.

The Three Steps of KYC Process

A good KYC process involves three main steps:

This involves collecting basic information about the customer, such as their name, address, date of birth, and identification number (e.g., Social Security Number). Banks must verify this information using reliable documents, such as government-issued IDs.

- Customer Due Diligence (CDD):

This step goes beyond mere identification. Banks assess the risk profile of each customer based on their financial activities, income sources, and overall financial behavior. There are three levels of CDD:

- Simplified Due Diligence (SDD): Applied to low-risk customers, involving basic identity verification.

- Standard Due Diligence: Applied to most customers, requiring a more comprehensive verification process.

- Enhanced Due Diligence (EDD): Applied to high-risk customers, such as politically exposed persons (PEPs) or those involved in high-value transactions. This involves deeper scrutiny and additional documentation.

- Ongoing Monitoring:

Continuous monitoring of customer transactions and activities to detect any suspicious behavior. This involves updating customer information regularly and reassessing their risk profiles.

Why KYC is Crucial in Banking

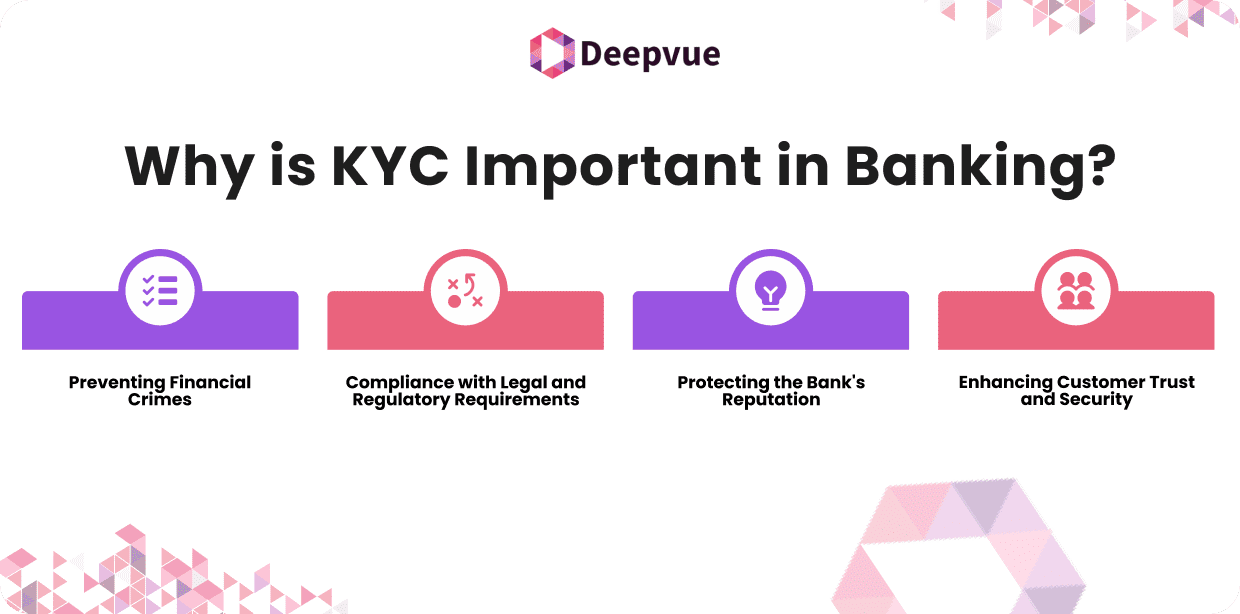

KYC plays a vital role in maintaining the integrity and security of the banking system. Here are the key reasons why KYC is essential:

1. Preventing Financial Crimes – The primary purpose of KYC is to prevent financial crimes such as money laundering, terrorist financing, and fraud.

By verifying the identity of their customers, banks can ensure that they are not dealing with individuals or entities involved in illegal activities. This helps protect the financial system from being exploited for criminal purposes.

2. Compliance with Legal and Regulatory Requirements – KYC is a legal requirement for banks, fintechs and financial institutions in most countries.

Regulatory bodies, such as the Financial Action Task Force (FATF), have established guidelines and standards for KYC to combat financial crimes globally.

Banks must comply with these regulations to avoid severe penalties, including fines and loss of operating licenses.

3. Protecting the Bank’s Reputation – A bank’s reputation is one of its most valuable assets. Failure to implement effective KYC procedures can lead to significant damage to their reputation.

Customers want to trust that their bank is secure and reputable. Any information about a bank’s involvement in financial crimes can erode customer trust and lead to a major business loss.

4. Enhancing Customer Trust and Security – KYC procedures help build trust between banks and their customers. When customers know that their bank takes security seriously and has measures in place to protect their identities, they feel more confident in their finances. This trust is essential for maintaining long-term customer relationships.

How Does the KYC Process Work?

The KYC process can vary slightly from bank to bank, but the fundamental steps remain consistent. Here’s a step-by-step process of how the KYC typically works:

1. Customer Identification

The first step in the KYC process is to identify the customer. This involves collecting basic information such as the customer’s name, address, date of birth, and identification number. Banks and fintechs require customers to provide valid identification documents, such as a passport, driver’s license, or national ID card.

2. Verification of Information

Once the customer’s information is collected, the bank verifies its authenticity. This involves checking the provided documents against official databases and other reliable sources. Some banks use advanced technologies such as biometric verification and facial recognition to enhance the accuracy of this process.

3. Risk Assessment

After verifying the customer’s identity, the bank conducts a risk assessment. This involves evaluating the customer’s financial behavior, transaction patterns, and source of funds. Based on this assessment, the bank categorizes the customer into a risk level (low, medium, or high).

4. Ongoing Monitoring

KYC doesn’t end with the initial identity verification. Banks continuously monitor customer transactions and activities to detect any suspicious behavior. This ongoing monitoring helps identify any changes in the customer’s risk profile and ensures compliance with regulatory requirements.

The Role of Technology in KYC

Advancements in technology have significantly improved the KYC process, making it more efficient and accurate. Here are some ways technology is transforming KYC in banking:

1. Digital Identity Verification

Digital identity verification involves using technology to verify a customer’s identity electronically. This includes methods such as biometric verification (e.g., fingerprint or facial recognition), document verification, and electronic signatures. Digital verification is faster and more accurate than traditional paper-based methods.

2. Artificial Intelligence (AI) and Machine Learning (ML)

AI and ML algorithms can analyze large volumes of data to detect patterns and anomalies that may indicate fraudulent activity. These technologies help banks automate the KYC process, reducing the need for manual reviews and minimizing the risk of human error.

3. Blockchain Technology

Blockchain technology provides a secure and transparent way to store and share customer information. It enables banks to verify customer identities without relying on a central authority. Blockchain also enhances data privacy and reduces the risk of data breaches.

4. eKYC

Electronic Know Your Customer (eKYC) is the process of verifying a customer’s identity electronically. In countries like India, eKYC has become popular due to the widespread use of digital identities such as Aadhaar. eKYC simplifies the onboarding process and reduces the need for physical documentation.

Challenges in Implementing KYC

Despite its importance, implementing KYC comes with several challenges. Here are some common challenges banks face in the KYC process:

1. Complex Regulatory Environment – KYC regulations vary across geographies. Banks & fintechs operating in multiple regions must know the complex regulatory requirements, which can be challenging and time-consuming. Ensuring compliance with all relevant regulations requires constant vigilance and adaptability.

2. Data Privacy Concerns – Collecting and storing customer information raises data privacy concerns. Banks & fintechs must ensure that they handle customer data securely and comply with data protection laws. Any breach of customer data can lead to severe legal and reputational consequences.

3. False Positives – KYC processes can sometimes generate false positives, where legitimate customers are flagged as suspicious. This can lead to delays in account opening and a poor customer experience. Banks need to balance stringent verification measures with minimizing false positives to maintain customer satisfaction.

4. Keeping Pace with Technological Advances – While KYC technology has become more accessible, keeping pace with technological advances remains a challenge. Implementing new technologies such as AI, blockchain, and biometrics requires significant investment and expertise. Banks must continuously upgrade their systems to leverage these technologies effectively.

5. Training and Expertise – Ensuring that staff are adequately trained to handle KYC procedures and understand evolving regulatory requirements is crucial. Banks need skilled personnel who can effectively manage KYC processes, detect suspicious activities, and ensure compliance with regulations.

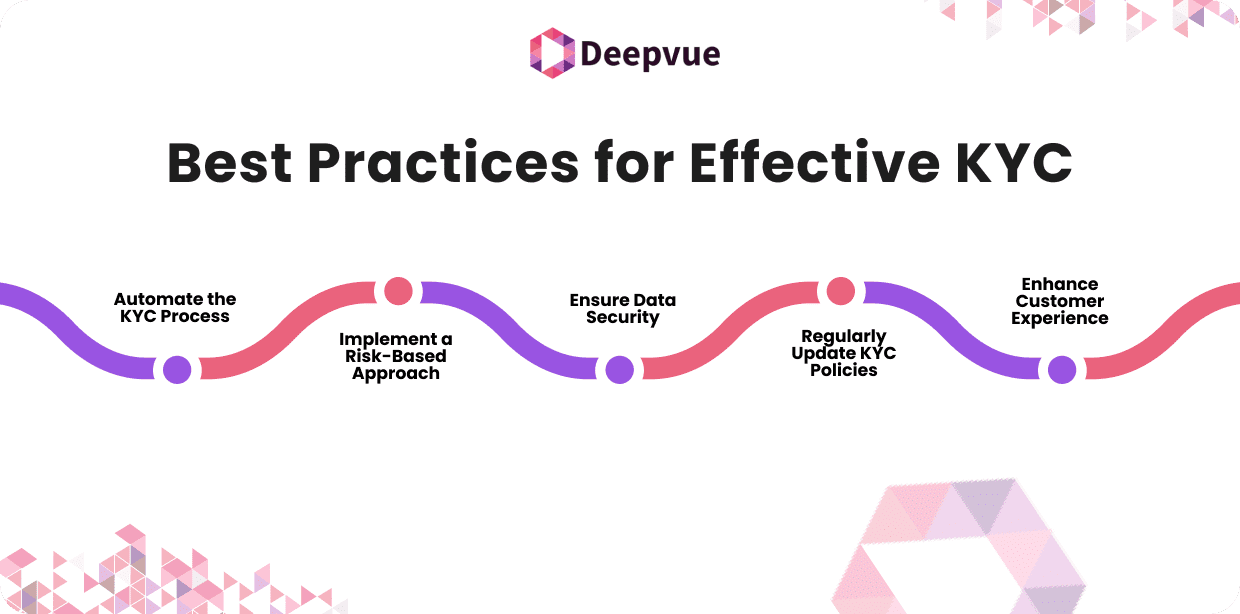

Best Practices for Effective KYC

To overcome the challenges and ensure an effective KYC process, banks can adopt the following best practices:

1. Automate the KYC Process

Automation can significantly enhance the efficiency and accuracy of the KYC process. Banks can use AI and ML algorithms to automate data collection, verification, and risk assessment. This reduces manual workload and minimizes the risk of human error.

2. Implement a Risk-Based Approach

A risk-based approach to KYC involves tailoring the level of due diligence based on the customer’s risk profile. High-risk customers require more stringent verification measures, while low-risk customers can undergo simplified due diligence. This approach ensures that resources are allocated effectively.

3. Ensure Data Security

Data security is paramount in the KYC process. Banks, fintechs must implement robust cybersecurity measures to protect customer data from breaches and unauthorized access. This includes encryption, secure storage, and regular security audits.

4. Regularly Update KYC Policies

KYC regulations and threats are constantly evolving. Banks must regularly review and update their KYC policies to stay compliant with the latest regulatory requirements and emerging risks. Continuous training for employees is also essential to keep them informed about the latest best practices.

5. Enhance Customer Experience

While KYC is a regulatory requirement, banks, fintechs should strive to make the process & customer journey as seamless as possible. This includes simplifying the onboarding process, providing clear instructions, and minimizing delays. A positive customer experience can enhance customer satisfaction and loyalty.

Conclusion

In conclusion, KYC in banking is a critical process that ensures the integrity and security of the financial system. By verifying customer identities and assessing their risk profiles, banks can prevent financial crimes, comply with regulatory requirements, and build trust with their customers.

Despite the challenges, adopting advanced technologies and best practices can enhance the efficiency and effectiveness of the KYC process. As the financial landscape continues to evolve, KYC will remain a cornerstone of secure and compliant banking operations.

To learn more about how Deepvue’s Identity Verification Suite can enhance the KYC verification process, visit Deepvue.tech and explore our range of APIs designed to ensure accuracy and efficiency.

FAQs

What documents are typically required for KYC?

Common documents required for KYC include government-issued photo IDs (like a passport or driver’s license), proof of address (such as a utility bill or lease agreement), and sometimes additional documents depending on the customer’s risk profile.

How often do banks need to update KYC information?

Banks are required to update KYC information periodically. The frequency of updated information can vary depending on the customer’s risk level. High-risk customers may require more frequent updates, while low-risk customers may only need updates every few years.

Can KYC be completed online?

Yes, many banks offer electronic KYC (eKYC) processes that allow customers to complete KYC online. This typically involves submitting digital copies of documents and may include biometric verification or video KYC for added security.

What happens if a customer fails to complete KYC?

If a customer fails to complete KYC, the bank may restrict or suspend their account until the process is completed. In some cases, the bank may be required to close the account to comply with regulatory requirements.

How does KYC help in preventing money laundering?

KYC helps prevent money laundering by verifying the identity of customers and assessing their risk profiles. By understanding the customer’s background and monitoring their transactions, banks can detect and report suspicious activities that may indicate money laundering.