The growth of e-commerce platforms in India has introduced a wave of change that serves the needs of various business requirements. The facilitation of smooth and safe payment processing is the pillar of a business. Whether it is online or offline, it is essential to choose the right payment processor far from payment errors, security attacks, and technical glitches.

Whether you’re a small business owner, an e-commerce platform, or a service provider, choosing the right payment processor is crucial for ensuring smooth transactions and customer satisfaction. This will have a significant impact on the company’s long-term profitability and can have repercussions for numerous aspects of the business.

In this post, we will discuss what is payment a processor and assist you in making the best decision for your company using this information.

Definition of Payment Processors

A financial organization or a third-party service provider that acts as go-betweens and safely moves money between the customer’s bank and the merchant’s bank is known as a payment processor. They accept digital payments from clients by using payment methods like UPI, debit cards, credit cards, and digital wallets. This ensures that the transaction is done securely without jeopardizing the safety of the user’s funds.

The main objective of the payment processor is to ensure that the money is transferred from the buyer to the seller at the time of purchase with the utmost speed and accuracy. They not only act as middleman but are also outfitted with cutting-edge security features including chargeback and fraud detection. Payment processors will transfer the money only when it is approved to improve transaction security. Payment processors in India must comply with the Payment Card Industry Data Security Standard (PCI DSS) and American Institute of Certified Public Accountants (AICPA) System and Organization Controls (SOC) regulations.

Payment Processors: How Do They Work?

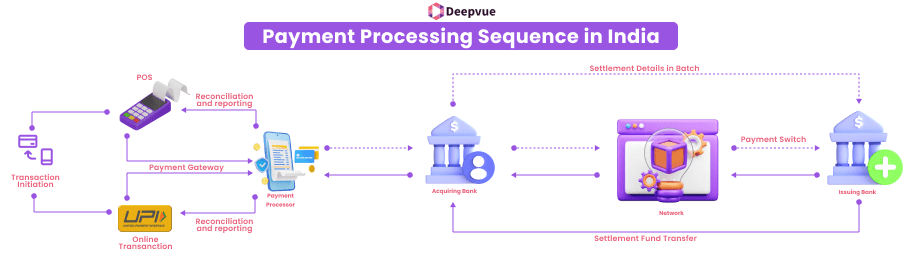

- The transaction is initiated when a customer pays through payment mediums like UPI, credit card, digital wallet, and debit card. Offline and online payments can be made using payment gateways, point-of-sale (POS) machines, e-commerce portals, and mobile applications.

- Once the customer has opted for a mode of payment, the merchant will encrypt the details of the transaction. This process will ensure the security and confidentiality of any pertinent information such as CVV, AVS verification, and others during transmission.

- Then, the encrypted information is sent to the customer’s bank or the issuing bank. After the bank receives the data from the payment processor, the bank will then verify whether the customer has sufficient funds for the transaction.

- After the bank confirms that there is enough balance in the bank account of the customer, it sends back an approved signal.

- To end the process, the payment processor will receive the authorization code from the acquiring bank. This code is then passed to the merchant and the order is completed. Now, the customer will receive a confirmation of the order.

Key Functions of Payment Processors

- Make Transactions Easier: During a transaction, the main responsibility of the payment processor is to receive the transaction details, encrypt them, and securely send them to the acquiring and issuing bank.

- Verifications and Authorisation: To ensure that the customer has sufficient funds available, the payment processor requests an authorization code from the issuing bank. It not only prevents fraud and unauthorized transactions but also verifies the validity of the payment method and the identification of the customer.

- Encryption and Security: Another key role of payment processors is to ensure compliance with security standards like PCI-DSS (Payment Card Industry Data Security Standard) to protect client information. To do this, direct payment processors use tokenization and encryption to securely exchange transaction information among the buyer, seller, and the banks or card network.

- Integration and Convenience: With payment processors, customers can make a purchase simply by using their smartphones. Payment processors in India provide a user-friendly interface and can integrate easily with your current POS system or shopping cart.

- Analytics and Reporting: To help businesses track sales, spot patterns, and improve business management, payment processors facilitate the retrieval of comprehensive reports. These reports provide insightful information on transaction data and improve your marketing and pricing strategies.

- Support for Multi Currencies and Payment Methods: Payment processors in India can receive payment in almost all types of currencies. Businesses can receive payment from around the world can get paid in their local currency.

- Detecting Fraud and Handling Chargebacks: Payment processors can offer advice and service to businesses in managing chargebacks and disputes. To reduce the vulnerability to fraud they use sophisticated algorithms and technologies to scan transactions for fraudulent behavior.

The Payment Processing Ecosystem

- Customer: The individual who is willing to purchase a product. For finalizing the transaction, the consumer will pass transaction information such as CVV, card number, expiration date, etc. to the payment processor.

- Merchant: Individual or business organization that is engaged in selling goods or services to the prospective purchaser. A payment processor, payment gateway, and merchant account are all requirements of the merchant.

- Merchant Account: This type of account is required for the merchant to receive payments from its customers. During a transaction, the merchant account is directly linked with the customer account, wherein the money is credited.

- Payment Gateway: The merchant website is connected to the payment processor through the use of a payment gateway. When the payment information of the customer is sent to the payment processor, the information is encrypted.

- Payment Processor: The main responsibility of the payment processor is to verify and authorize the payment information of the customer. Additionally, it communicates with banks of both the customer and the merchant’s bank to close the transaction.

Factors to Consider When Selecting a Payment Processor

- Pricing Structures: For businesses willing to choose a payment processor in India and across the globe, it is important to thoroughly understand the fee structure. Most payment processor providers charge transaction fees, chargeback fees, setup fees, monthly fees, and currency conversion fees. Thus, one should select the perfect payment processor that will suit your business growth, objectives, and volume of transactions well.

- Sales Volume Factors: In sales volume considerations, companies have to balance between those direct payment processors charging lower fees but taking longer time to process and higher-fee-charging ones that give immediate processing. Selecting the right payment processor depends on the specific needs and priorities of the business.

- Compatibility with Business Type: Payment processors in India and worldwide have limitations for particular types of businesses. Therefore, it is important to ensure that the payment processor you choose is compatible with your business type. When selecting a payment processor, make sure that it is suited to your business type and meets the needs of your business.

Popular Payment Processors in India

The following are the most popular payment processors in India:

- Paytm Payment Gateway

- Razorpay

- PhonePe

- PayU

- Cashfree Payments

- Amazon Pay

Conclusion

Payment processors have revolutionized the way Indian businesses process transactions, offering seamless, secure, and convenient payment solutions. As companies expand, the payment processor is chosen based on certain factors, balancing transaction speed, fees, and reliability to suit specific requirements.

Also, APIs such as Bank Account Verification API and UPI ID Verification API augment the payment ecosystem. Our Bank Account Verification API provides for safe and authentic verification of banking details, mitigating errors and fraud while affecting transactions. Likewise, our UPI ID Verification API eases the task of verifying UPI IDs, allowing for hassle-free and efficient peer-to-peer or merchant transactions.

By using the appropriate payment processors and incorporating advanced verification tools, businesses can streamline their operations and improve customer satisfaction.

FAQ:

Is UPI a payment processor?

No, UPI is not a payment processor. UPI is an instant payment system created by the National Payments Corporation of India (NPCI) that facilitates the transfer of funds between bank accounts instantly via a mobile platform.

What is a payment gateway?

A payment gateway is software that serves as an intermediary between a merchant’s application or site and the payment processor. It encrypts and safely captures customer payment information (like credit card details) and sends it over to the payment processor for authorization.

What is a payment gateway vs a payment processor?

A payment gateway is a front-end technology that gathers and encrypts consumer payment data and passes it through to the payment processor. It serves as the intermediary between the customer, merchant, and processor. A payment processor is the back-end service that speaks with the customer bank and merchant bank to verify and settle the transaction. It is responsible for the actual transfer of money.

How does a payment gateway ensure information security?

Payment gateways employ strong security practices to secure sensitive customer data, such as encryption, tokenization, PCI DSS Compliance, and fraud detection mechanisms to identify fraudulent transactions and stop them.

What is a payment processor?

A payment processor is a service that makes it possible for a customer’s bank and a merchant’s bank to transfer funds from the customer to the merchant during a transaction. It processes the authorization, settlement, and transfer of payments so that the merchant can be paid efficiently and securely.