Small and Medium Enterprises (SMEs) form the backbone of India’s economic activity, fueling innovation, jobs, and economic growth. Timely and sufficient access to finance continues to be a lingering issue for these businesses. SME lending platforms have become the crucial enablers, filling the gap between conventional financial institutions and unserved enterprises. They use technology to enable instant, hassle-free access to working capital, term loans, and invoice financing, addressing varied business requirements.

From new-age fintech platforms to traditional non-banking financial companies (NBFCs), the SME lending market in India is transforming at a tremendous pace. This guide takes a closer look at the best SME lending platforms in India, their special features, eligibility, loan products, and how they enable small businesses to grow and become successful.

Introduction to SME Lending in India

SME lending is the financing service that is specially formulated for small and medium-sized businesses. The loans are in different forms, such as working capital loans and business loans, and are crucial to furnish funds to startups and mature businesses. The loans are underwritten by banks and fintech institutions and usually are in the form of collateral to facilitate lending.

Role of Digital Lending Platforms

Digital lending platforms have revolutionized SME lending in India with quicker, collateral-free loans via alternative data such as GST returns and bank statements. They fill the ₹25 lakh crore credit gap with accessible, technology-led solutions such as TReDS for invoice discounting. Sophisticated technologies facilitate rapid loan disbursals, enhancing access to credit for disadvantaged SMEs. Intuitive interfaces simplify the application process, making borrower experience better. Government programs such as GST Sahay and the Credit Guarantee Fund facilitate SME financing further.

Key Platforms Facilitating SME Lending

Chola SME

Chola SME Loans provide tailored financial solutions to small and medium enterprises (SMEs) for business expansion, working capital, and asset acquisition. They provide collateral-free loans, loan tenures that can be flexed, and rapid disbursal to address the varied credit requirements of SMEs.

Lendingkart

Lendingkart provides online lending solutions to SMEs emphasizing convenient access to working capital loans. The company utilizes data analysis and technology to evaluate creditworthiness in a short time, facilitating instant approval and disbursal of loans without collateral.

FlexiLoans

FlexiLoans is focused on extending unsecured loans to SMEs with a flexible repayment pattern. The company provides business loans, line of credit, and vendor financing to assist small businesses in having sufficient cash flow and effectively managing operational costs.

Specialized Lending Solutions

GST Sahay: Simplifying GST-based Lending

GST Sahay is an online lending program aimed at extending instant working capital loans to GST-registered micro, small, and medium enterprises (MSMEs) based on their GST information. With GST returns, lenders can evaluate the creditworthiness of borrowers more precisely and release funds promptly without security. It simplifies the lending procedure and facilitates financial inclusion for GST-registered MSMEs.

TReDS: Invoice Discounting Explained

TReDS (Trade Receivables Discounting System) is an online platform that allows MSMEs to discount their trade receivables to financial institutions at a discounted rate. By discounting bills raised against large corporate buyers, MSMEs are able to receive immediate funds to sustain cash flow while financial institutions are able to get a return on discounted bills. It reduces payment delay and increases the liquidity of MSMEs.

CGTMSE: Credit Guarantee Schemes

Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) is a government-backed scheme that provides collateral-free credit to micro and small enterprises (MSEs). It encourages lenders to lend without collateral as a part credit guarantee on loans, splitting the risk with financial institutions, and enabling MSEs’ access to finance.

Government Initiatives Supporting SMEs

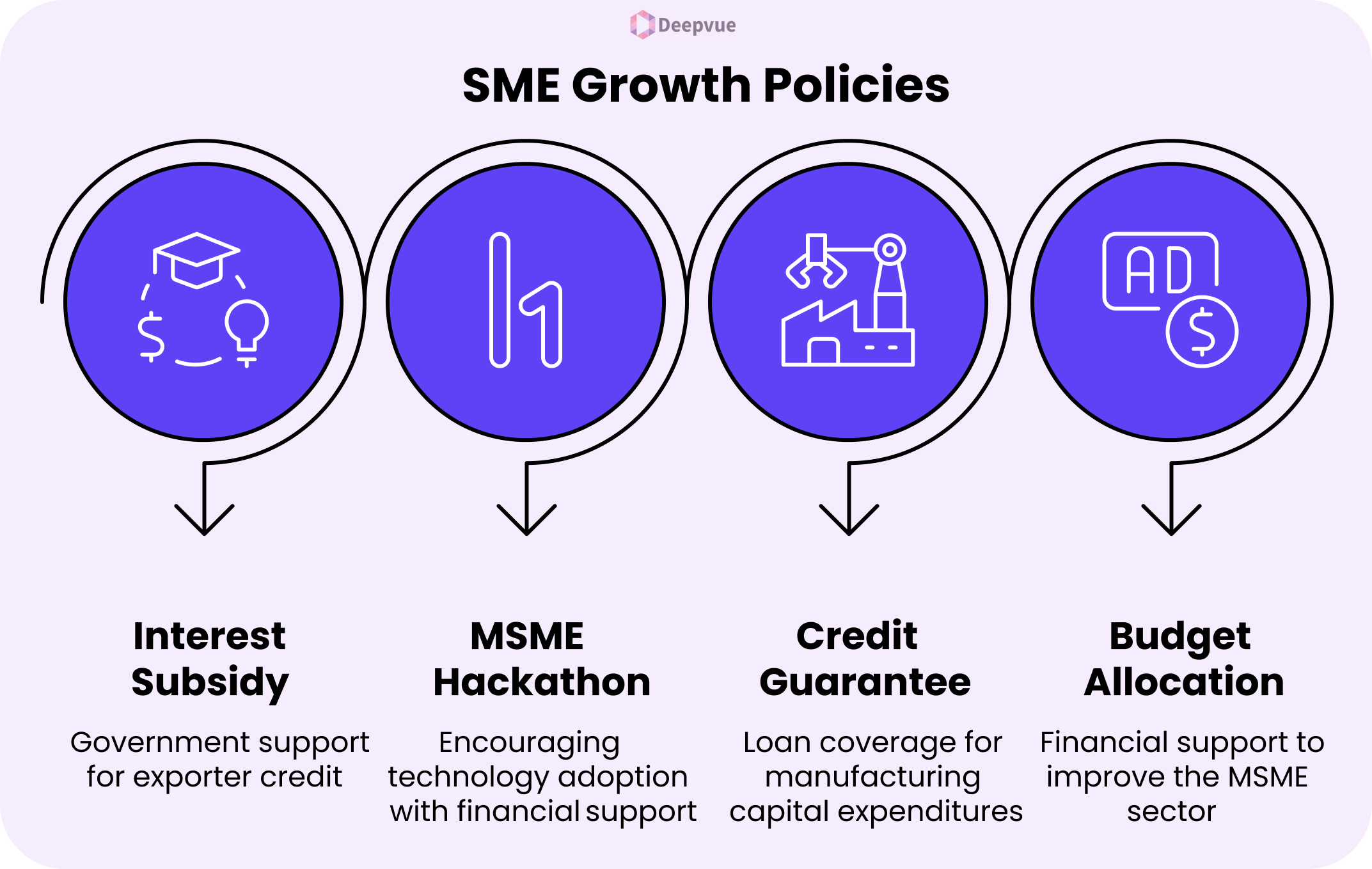

Recent Policies Encouraging SME Growth

- Interest Subsidy to Exporters: The government is contemplating introducing an interest subsidy on credit to exporters, specifically favoring MSMEs, to promote their international competitiveness.

- MSME Hackathon 4.0: Initiated to encourage the embracement of advanced technologies among MSMEs, aiding them in design, strategy, and implementation, and offering financial support to young entrepreneurs.

- Credit Guarantee Scheme for Manufacturing MSMEs: Launched to enable term loans for manufacturing MSMEs with up to ₹100 crore cover for capital expenditures.

- Budget 2024-25 Allocation: The Union Budget 2024-25 provided ₹22,137.95 crore to improve the MSME sector through specially targeted actions such as increased credit guarantees and better loan access.

Public-Private Partnerships in Lending

- Collaboration with Fintech Startups: Major public sector banks are considering collaboration with fintech startups to boost lending to MSMEs, to speed up credit flow to the segment.

- E-commerce Export Hubs: The government intends to set up e-commerce export hubs under PPPs for easy access to international markets for MSMEs as well as traditional craftspeople.

- Infrastructure Development: With PPPs, the government, banks, and NBFCs are investing in infrastructure development to facilitate the MSME sector and provide necessary assistance for business growth.

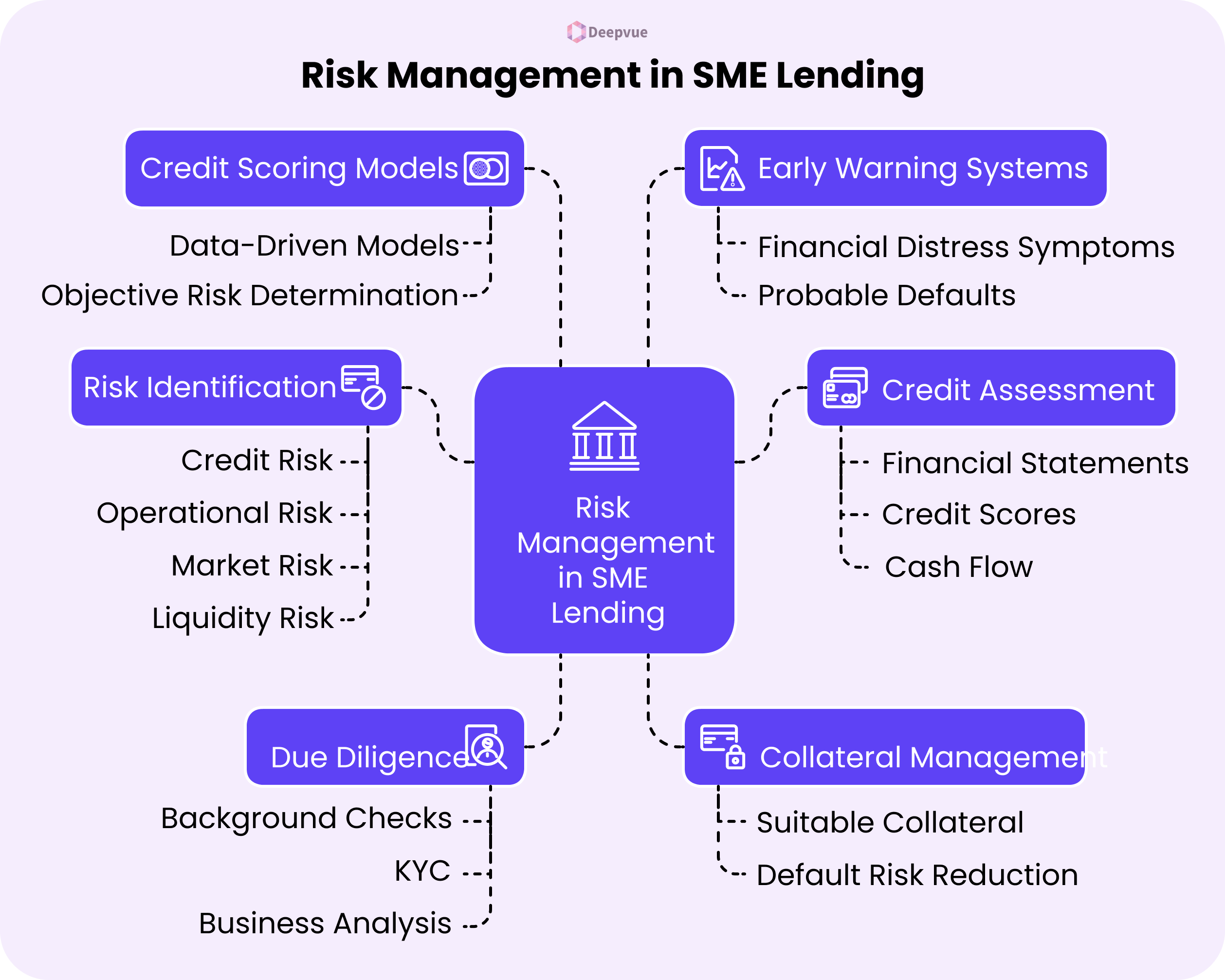

Risk Management in SME Lending

- Risk Identification: Determine the risks, like credit risk, operational risk, market risk, and liquidity risk, applicable to SME borrowers.

- Credit Assessment: Analyze the creditworthiness of the borrower from financial statements, credit scores, and cash flow.

- Collateral Management: Manage secure loans with suitable collateral to reduce default risk.

- Credit Scoring Models: Use data-driven credit scoring models to determine borrower risk objectively.

- Due Diligence: Perform thorough due diligence, such as background checks, KYC, and business analysis.

- Early Warning Systems: Create early warning systems to identify symptoms of financial distress and probable defaults.

Strategies for SMEs to Enhance Financial Operations

- Adopt Cash Flow Forecasting: Develop accurate cash flow projections to anticipate financial gaps and plan effectively.

- Automate Payment Processing: Implement automated payment systems to speed up payments and enhance the management of cash flow.

- Optimize Inventory Management: Install inventory tracking systems to minimize surplus stock and preserve liquidity.

- Watch Financial KPIs: Keep an eye on financial stability indicators such as profit margins, liquidity ratios, and receivables turnover.

- Leverage Tax Incentives: Use government tax incentives, grants, and subsidies to reduce expenses.

Conclusion and Future Prospects of SME Lending in India

SME lending in India is poised to grow enormously and change with the increasing acceptance of digital modes, regulatory measures, and more innovative financing opportunities. In the future, it is anticipated that the adoption of new technologies such as AI, machine learning, and blockchain technology will further mechanize credit checking and increase transparency. Also, increased partnership between fintechs, banks, and government programs will create an inclusive financial environment. The future of Indian SME lending is full of great promise, with new possibilities for businesses to raise capital, expand with confidence, and define the shape of India’s entrepreneurial future.

FAQ

What are SMEs in India?

SMEs (Small and Medium Enterprises) in India refer to enterprises with limited size in the context of investment and turnover, and these play a crucial role in employment as well as economic growth in various sectors.

How to Apply for SME Loans in India?

You can apply for SME loans from banks, NBFCs, or online lending platforms by providing required documents such as business proof, financial statements, and identity proof, after which the loan is approved and disbursed.

What to note before availing a business loan?

Assess the loan amount, rate of interest, repayment term, processing charge, and your business’s repayment ability before agreeing on a business loan.

Why are existing lending protocols difficult for SMEs?

Existing lending protocols tend to include lengthy procedures, tight collateral requirements, and poor credit history, which render most SMEs unable to secure timely financing.

Why is SME Lending Significant?

SME lending drives business expansion, innovation, and employment generation, enabling small businesses to overcome financial constraints and make significant contributions to the economy.