Financial institutions bank on strong systems to identify and block illegal activities, including money laundering, fraud, and financing of terrorism. Two key elements of these systems are transaction screening and transaction monitoring—two seemingly similar words that have different applications within the compliance regime. Although transaction monitoring and screening are used to protect financial ecosystems against risk, they function at different points and incorporate different mechanisms.

It is crucial that compliance teams and fintech platforms understand how these two processes are different, yet also how they complement each other. This post analyzes the differences between transaction monitoring and transaction screening and discusses how they complement each other to strengthen anti-money laundering (AML) initiatives.

Defining Transaction Screening

Transaction screening is the process of checking financial transactions against predefined criteria—such as watchlists, sanctions lists, or blacklists—before they are executed. Its objective is to identify and block transactions related to high-risk individuals, entities, or countries.

Core Features of Transaction Screening

- Sanctions List Checks: Compare transaction information with worldwide sanctions and PEP (Politically Exposed Persons) lists.

- Name Matching Algorithms: Employ fuzzy logic to find close matches to known risk parties.

- Real-time Checks: Monitors transactions in real time to prevent high-risk behavior.

- Custom Rules: Enables companies to create specific risk parameters according to their needs for compliance.

Preventive Function of Screening

Transaction screening serves as a first line of defense by inhibiting or marking high-risk transactions prior to execution. It assists in helping the financial institutions avoid regulatory breaches, financial crimes, and reputational loss. Screening ensures compliance and improves overall risk management by preventing suspicious activity early.

Use of Watchlists in Screening

Watchlists are lists of names of persons, parties, or nations engaged in or suspected of engaging in illegal activity, terrorism, or sanctions violations. Transaction screening software compares transaction information (e.g., sender/receiver names) against watchlists to determine and suspend or alert suspicious transactions. Typical watchlists are OFAC, FATF, Interpol, and local regulatory agency lists.

Defining Transaction Monitoring

Transaction monitoring refers to the ongoing surveillance of financial transactions to detect patterns or behaviors that may indicate suspicious activity, such as money laundering or fraud, often after the transaction has occurred. It is a key component of Anti-Money Laundering (AML) and fraud prevention programs.

Real-time Analysis in Monitoring

Real-time transaction monitoring entails reviewing transactions as they happen. This allows financial institutions to identify and act in real-time against high-risk activity, to prevent fraud or regulatory violations from occurring. These activities include unusually large transactions, abrupt shifts in transaction patterns, or transactions with high-risk destinations.

Historical Data Analysis in Monitoring

Historical data analysis is the process of examining historical transaction data to detect patterns, trends, and anomalies over time. It helps to enhance risk models, detect long-term suspicious behavior, and aid in investigation by providing context to recent behavior.

Role in Ensuring Regulatory Compliance

Transaction monitoring is an important function in ensuring financial institutions comply with regulations such as AML and Counter-Terrorism Financing (CTF) legislation. Monitoring systems are required by regulators to identify and report suspicious transactions (e.g., filing Suspicious Transaction Reports or STRs), and having an effective monitoring process assists institutions in preventing legal fines and reputational risk.

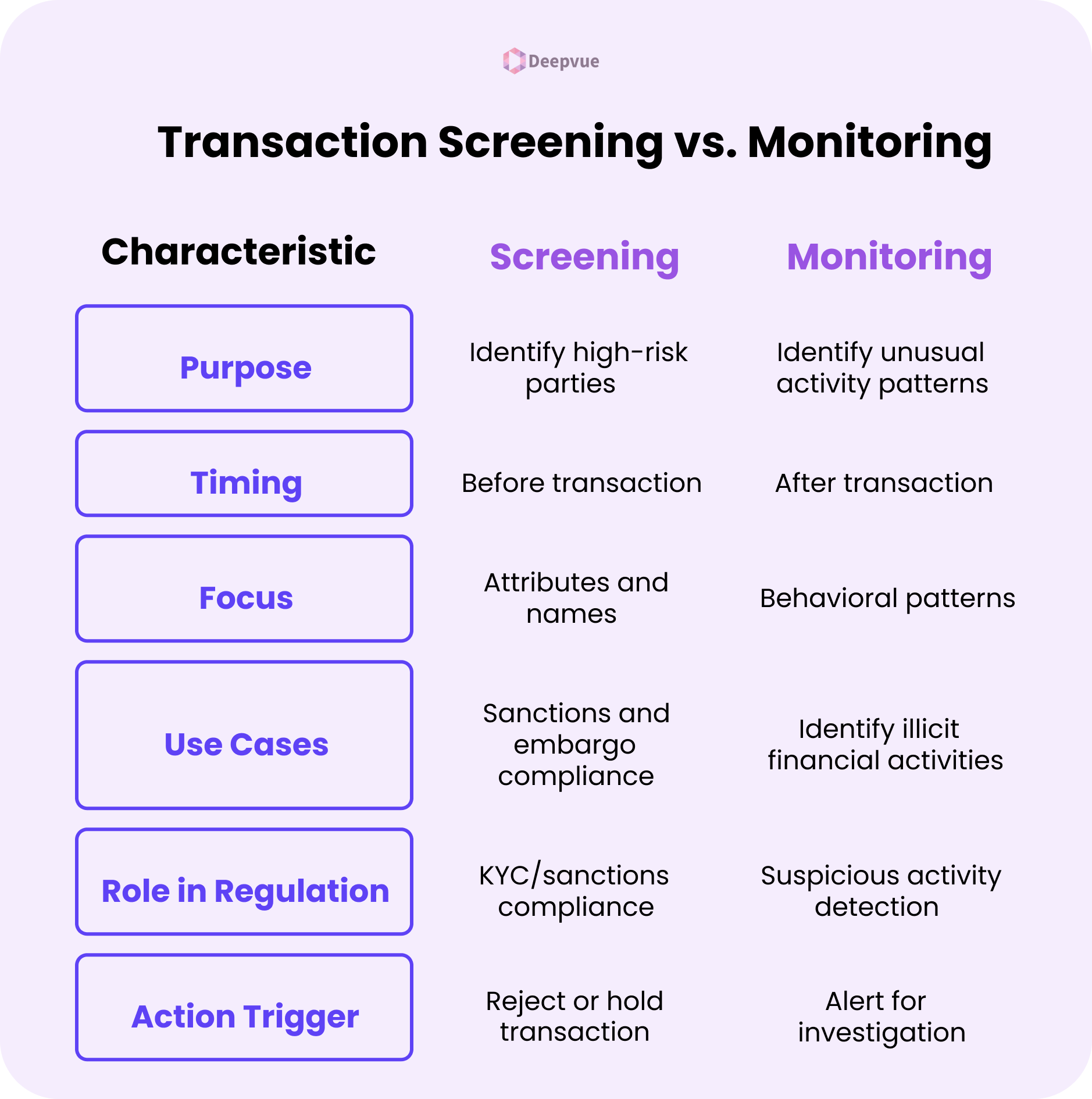

Comparative Analysis: Transaction Screening vs Transaction Monitoring

Purpose

- Transaction Screening verifies transactions in real time prior to processing, mainly to identify high-risk parties (e.g., sanction targets, countries, or PEPs).

- Transaction Monitoring regularly reviews completed transactions after the fact to identify unusual patterns of activity or behavior (e.g., fraud or money laundering).

Timing

- Screening is done in advance of a transaction.

- Monitoring is done after a transaction has taken place or on an ongoing basis.

Focus

- Screening concentrates on attributes and names (such as sender/receiver, banks, countries) against watchlists and blacklists.

- Monitoring is a behavioral pattern focused (e.g., volume, frequency, deviance from a customer’s normal behavior).

Use Cases

- Screening is typically used to meet sanctions and embargo compliance.

- Monitoring is applied to identify money laundering, terrorist financing, and fraud.

Role in Regulation

- Transaction monitoring and screening are necessitated by AML regulations, but screening refers to KYC/sanctions compliance, whereas monitoring assists with suspicious activity detection.

Action Trigger

- Screening can reject or hold the transaction pending clearance.

- Monitoring triggers an alert for investigation or reporting (e.g., SAR filing).

With the pace of digital transformation accelerating and cyber-financial crime becoming more advanced, rates of fraud globally rose from 13% in 2021 to 16% in 2022. The sudden spike identifies the critical need for advanced transaction monitoring systems in all financial institutions.

How do Screening and Monitoring Complement Each Other?

Screening is the first line of defense through excluding transactions with high-risk or offending individuals. Monitoring provides the second layer by examining the pattern and behavior in sound offending transactions that could be indicative of financial crime. Combined, transaction monitoring and screening assist financial institutions in ensuring regulatory compliance, preventing money laundering, fraud detection, and minimizing operational risks. While screening automatically blocks known threats, monitoring identifies emerging and changing typologies of financial crime.

Challenges in Transaction Screening

- Dealing with False Positives: Transaction screening software tends to produce a large number of false positives—genuine transactions flagged mistakenly as suspicious. These cause operational inefficiencies, processing delays, and elevated workload for compliance teams. High volumes of false positives may also contribute to customer dissatisfaction and business relationship strain.

- Managing False Negatives: False negatives refer to situations where truly suspicious or illegal transactions remain undetected. These are of grave regulatory, legal, as well as reputational risks for financial organizations. Failure to detect such transactions can lead to non-compliance with anti-money laundering (AML) and counter-terrorist financing (CTF) rules.

Challenges in Transaction Monitoring

- Issues with Real-time Data Processing: It is technologically demanding and resource-intensive to process huge amounts of transactions in real time. High-speed infrastructure and sophisticated algorithms are needed to identify suspicious patterns in real time without creating any delay in legitimate transactions.

- Integration with Current Systems: Most financial institutions have legacy systems that are not very compatible with current monitoring systems. New monitoring systems for transactions typically involve much customization, significant cost, and potential disruptions of existing operations.

The Role of Advanced Technology

Emerging technologies such as Artificial Intelligence (AI) and Machine Learning (ML) are absolutely essential for improving transaction monitoring and screening processes. Artificial intelligence algorithms are able to process enormous amounts of data quickly, detect patterns, and mark unusual activity faster and more accurately than humans. This is particularly crucial in the case of detecting fraudulent transactions, suspicious account behavior, and potential risks of money laundering.

Increasing Accuracy and Efficiency

Artificial intelligence tools eliminate human mistakes and better ascertain risk detection with enhanced accuracy. The systems can analyze real-time data streams, allowing for faster decision-making and proactive measures. This maximizes operational efficiency while maintaining regulatory compliance.

The Synergy between Screening and Monitoring

When screening (upfront risk assessment) and monitoring (ongoing supervision) are used together, they create a powerful defense against financial danger. Screening prevents onboarding the risky one-off, while monitoring is always on the lookout for behavior to identify potential emerging risks. They form a layered risk management strategy together.

- Collective Impact on Risk Management: The convergence of AI-based screening and monitoring enhances the ability of an organization to manage financial, reputational, and compliance risks. With the integrated approach, institutions are better positioned to anticipate changing threats and regulations.

- Decreasing Financial Crimes: Through the ability to detect and respond in real time, emerging technology greatly minimizes the occurrences of fraud, money laundering, identity theft, and other financial crimes. With advancements in the systems, not only are institutions safeguarded, but the overall trust within the financial system also increases.

Conclusion

Though transaction monitoring and screening play distinct roles, both are crucial foundations of an effective financial crime prevention strategy. Screening is the initial defense by identifying high-risk transactions before they take place, whereas monitoring ensures ongoing control to identify patterns of suspicious activity over time. These combine to make a holistic approach to compliance and risk management.

This is where our bank statement analysis API comes in. Further pushing the boundary of the framework, our API extracts and analyzes financial data in real-time from bank statements, giving a deeper view into a customer’s transaction pattern, income consistency, and spending behavior. Moreover, the incorporation of such detailed financial information enhances decision-making and the effectiveness of preventive and investigative AML controls.

FAQ

What is transaction screening?

Transaction screening is the method of screening transactions in real-time against watchlists, PEPs, and sanctions lists to avoid high-risk payments from reaching their destinations.

What is transaction monitoring?

Transaction monitoring entails reviewing customer transactions in a temporal manner to determine unusual or suspicious activity that can signal money laundering or fraud.

How do transaction screening and monitoring differ?

Screening happens before a transaction is completed and focuses on specific risk lists, while monitoring occurs post-transaction and looks at patterns over time.

Why are both processes important in AML compliance?

Both are critical—screening blocks known threats immediately, and monitoring detects hidden or evolving risks that require deeper analysis.

What are common red flags in transaction monitoring?

Unusual transaction volumes, frequent large cash deposits, and transactions inconsistent with customer profiles are common red flags.