Debt. The word itself is so powerful that it can make someone feel uneasy. Be it an unpaid loan, or a stack of overdue credit card bills, it is something that most of us wish to avoid having a conversation about. But what happens when debts go unpaid for too long?

The debt collection process is a structured way to settle things amicably and fairly. For business, it is about maintaining the cash flow. Well, for consumers it is often a reminder of bills piling up faster. And for debt collection agencies? Well, they’re like the middlemen trying to keep the peace between money owed and money collected with a little fee and effort included.

In this blog, we’ll understand what is debt collection process, demystify how it works, and show you why it’s more than just sending stern letters.

What is the Debt Collection Process?

Having debt is common but certainly not wise for business owners. If you ignore it, your business might face heavy repercussions, including repossession, bankruptcy, eviction, lower credit score, foreclosure, and more. Here comes debt collection, a process by which third-party debt collectors or lenders attempt to collect the money owed by individuals or businesses.

The debt collection process for small businesses and enterprises starts once the borrower has missed 2-3 or more EMIs. The lending companies will give gentle reminders like messages, calls, emails, and letters to the borrower to understand the issue and provide a solution accordingly. If and only if the borrower refrains from responding or making any payment, then third-party agencies will get involved followed by legal actions. The lending companies will collaborate with the third-party debt collectors so that they can help in recovering the debt amount.

One important thing to note is that lending companies will never hound the borrowers as they are regulated by the Consumer Financial Protection Bureau (CFPB) and the Fair Debt Collection Practices Act (FDCPA). These regulations protect the borrowers from unfair practices and harassment from the lending institutions.

Do You Know Your FDCPA Rights?

The Fair Debt Collection Practices Act (FDCPA) is a federal law intended to safeguard consumers from the rapacious process of collecting debt. This act refrains the debt collectors from practicing aggressive or dishonest means of collecting outstanding debt. The act includes the following:

- The debt collecting agencies can reach out to you from 8 am to 9 pm. They may not call you at odd times or locations.

- They cannot contact you publicly on social media regarding your unpaid balance. If you don’t ask them to stop, they can still send you private messages.

- It is illegal for debt collectors to harass customers, use obscene language, or make threats.

- The agency must cease contacting you and get in touch with the lawyer if you decide to seek legal counsel to handle the debt. But you have to provide the agency with the name and contact details of your lawyer.

- If the debt collecting agency is pursuing any illegal practice then you can file a complaint with the Consumer Financial Protection Bureau, Federal Trade Commission, or the attorney general of your residing state.

- Any debt collector attempting to conduct misleading practices then one can sue them in federal court.

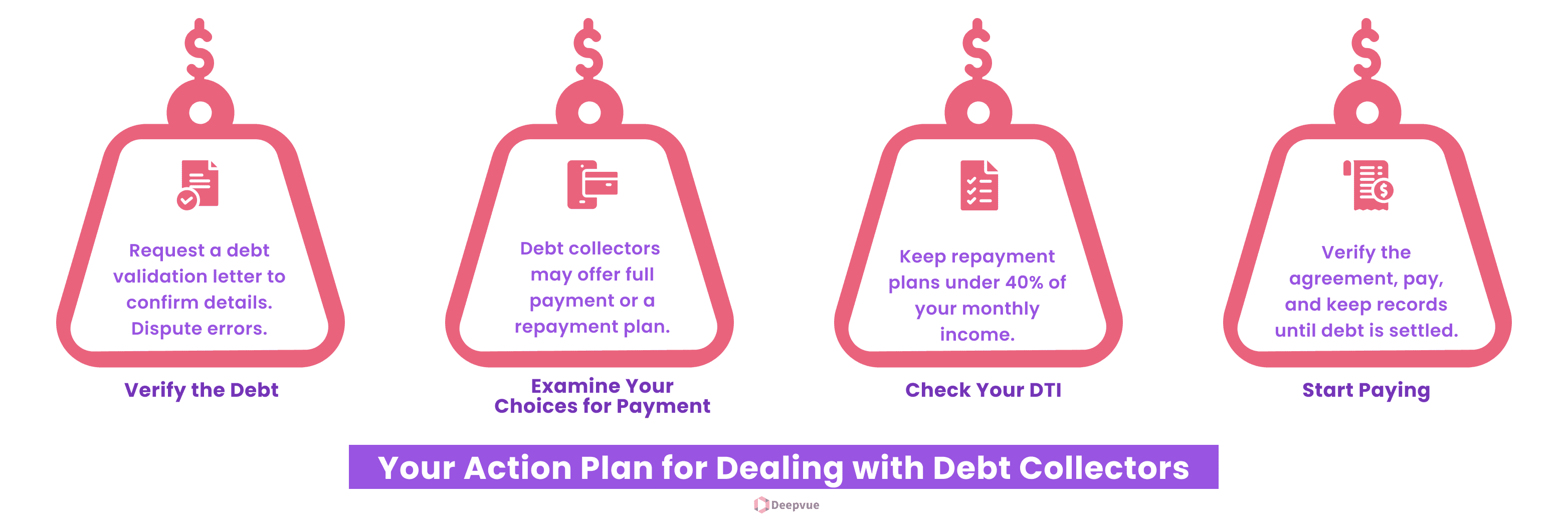

Your Action Plan for Dealing with Debt Collectors

- Verify the Debt

Before making any payment you must receive a debt validation letter from the debt collection agency. This letter acts as a confirmation of whether the outstanding amount is yours or not. It will have information like the debt amount, creditor details, and type of debt, among other things. In case, you find any errors or you fail to recognize the debt then you must raise a complaint within the first 30 days.

- Examine Your Choices for Payment

In most cases, the debt collector will offer two modes of payment options. You can either pay the full amount or have a new repayment plan. The best course of action will be determined based on the outstanding debt and your budget. There might be a chance for you to have a decent repayment plan that is less than what you owe.

- Check Your DTI

While negotiating your repayment plan, first calculate your debt-to-income ratio. Your monthly payment should not exceed 40% of your monthly income. It is wise for a consumer to calculate their DTI beforehand.

- Start Paying

Before making any payment ask for a formal agreement with the debt collector. Once you receive the agreement thoroughly check for the details for accuracy. After verifying the details you can start repaying your debts. Confirm with the collector once your initial payment goes through. Maintain a record of each payment you make. Once an agreement is reached or the debt is settled, the case is closed.

Bringing It All Together

The debt-collecting process is one legal way of collecting overdue debts. The process is structured and often governed by law. It is an essential tool for creditors to receive the outstanding payment from their borrowers. Given its importance, debt collectors need to abide by the law and stick to moral behaviors by threatening debtors fairly. The lawful goal of debt collectors and collection agencies is to assist creditors in recouping at least some of the money they are due. Numerous rights for debtors are outlined in the Fair Debt Collection Practices Act, which also specifies some rights for debt collectors.

Recovering a debt is a task, therefore the best way is to refrain from having any debt. In case, you happen to have any debt then make contact with the lender to receive an adequate solution. The best way to keep the debt collecting agencies is to make your credit card and other payments on time. Need help navigating the complexities of debt collection? Reach out to our experts for customized solutions and professional advice.

FAQ:

What is the debt collection process?

The debt collection process refers to the measures taken by the creditors or agencies to recover unpaid debts. It involves reminders, negotiations, and sometimes legal action to settle outstanding payments.

How long does a creditor wait before starting the debt collection process?

Most creditors start the debt collection process after 30-90 days of non-payment, depending on the terms of the agreement.

Can I negotiate with a debt collector?

Yes you can, by negotiating the payment term, settlement for a smaller amount, or setting up a payment plan to ensure you settle your debt

Will unpaid debts affect my credit score?

Indeed, when the debt collected is reported to the various credit bureaus, they may lower one’s credit score and stay for up to seven years.

What happens if I ignore a debt collector?

In most cases, ignoring a debt collector leads to additional fees, and legal action, or impacts your credit score negatively. It is better to deal with the matter at once.