Re-KYC (Re-Know Your Customer) is a compliance exercise that financial institutions have to undertake periodically to verify that customer details are up to date and correct. In the case of medium-risk customers—those between low and high risk in terms of profile and transaction behavior—regulatory authorities make it compulsory to re-verify every now and then, say every two years. This demand is not solely a compliance gesture; it is an integral aspect of risk handling, fraud combating, and maintaining the integrity of the financial sector.

Understanding Re-KYC

Re-KYC (Re-Know Your Customer) is the periodic process of updating and verifying a customer’s personal, professional, and compliance-related information. It ensures that customer records remain accurate, relevant, and in line with regulatory requirements over time.

Medium-risk customers often include individuals or entities with moderate transaction volumes, international exposure, or slightly complex financial relationships. While not immediately high-risk, their profiles necessitate closer scrutiny over time. The banks and other financial institutions need to have efficient, customer-friendly Re-KYC operations that strike the right balance of regulatory requirements against low customer resistance.

Importance of Maintaining Up-to-Date Information

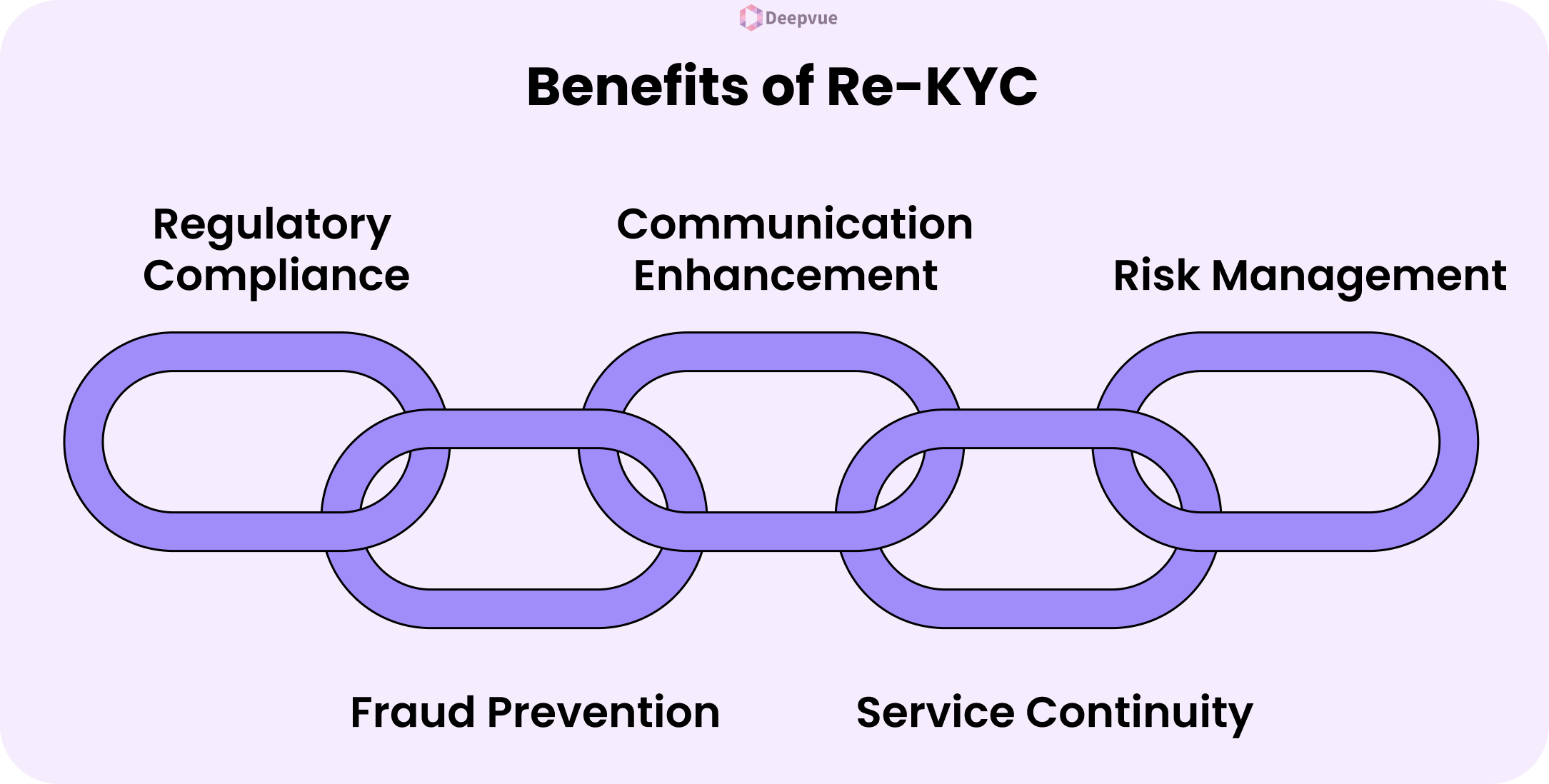

- Re-KYC helps financial institutions comply with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations.

- It minimizes the risk of fraud by verifying the customer’s name and contact information.

- It ensures that institutions remain in touch with customers through smooth communication using updated contacts.

- Re-KYC is important to avoid disconnection of banking and financial services because older information may cause restrictions on the account.

- It supports better risk management and customer profiling for personalized service offerings.

Medium Risk Customers Explained

Know Your Customer(KYC), medium-risk customers are individuals who present a moderate level of risk to financial institutions in terms of money laundering, fraud, or identity misuse. These customers are usually not high-risk red flag ones, but need more monitoring than low-risk customers. Medium-risk customers are, as part of the Re-KYC (Re-Know Your Customer) process, subject to regular updates and increased monitoring than low-risk profiles.

Criteria for Medium Risk Classification

- Customers with inconsistent or incomplete KYC information.

- Those with a moderate number of transactions that are not entirely consistent with their declared profile.

- Customers from areas with limited regulatory controls or politically volatile regions.

- Infrequent cash transactions or third-party account usage.

- Those with a history of delayed documentation or suspicious but non-criminal activity.

- Small- or medium-sized enterprises in industries that are likely to face moderate risk (i.e., import-export, freelance services).

Risks Associated with Medium-Risk Customers

- Risk of identity abuse as a result of incomplete or expired documentation.

- Risk of structuring or layering transactions to conceal.

- Exposure to moderate fraud attempts, especially through third-party manipulation.

- Possibility of regulatory breaches due to gaps in customer data or due diligence.

- Reputational risk if the customer is later found to be involved in financial misconduct.

The Re-KYC Process

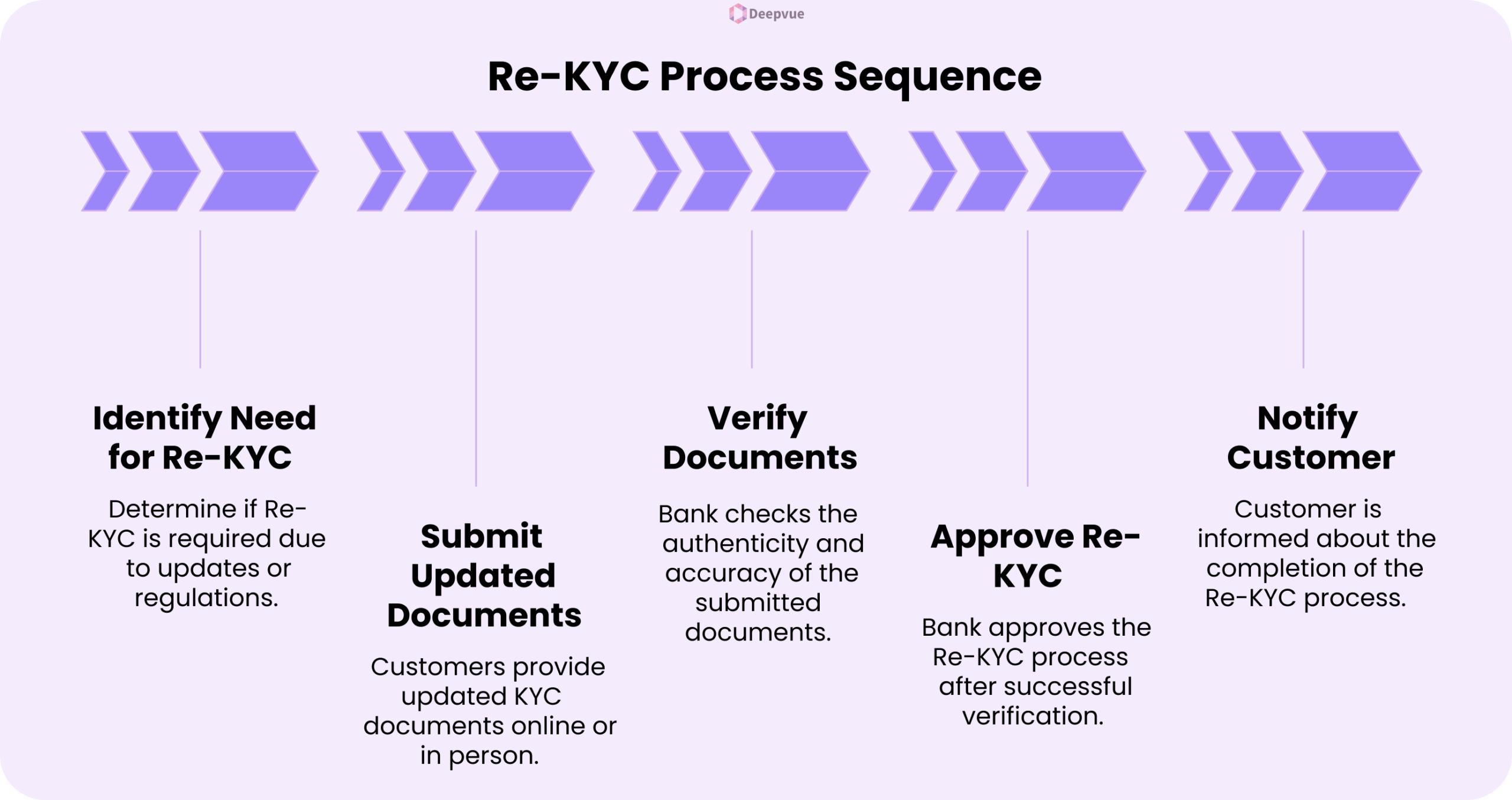

When Re-KYC Becomes Necessary?

Re-KYC is normally called for whenever there are updates in a customer’s personal details (such as address or name), or as per periodic recommendations specified by regulatory guidelines to avoid fraudulent activities and ensure compliance.

Submitting Re-KYC Documents

Customers can submit updated KYC documents—such as proof of identity and address—either online through the bank’s portal or app, or by visiting a branch in person.

Verification and Approval

After submitting documents, the bank checks the information for authenticity and accuracy and, after successful verification, notifies the customer of Re-KYC completion.

Enhanced Due Diligence (EDD) for Medium Risk Customers

Enhanced Due Diligence (EDD) is an increased level of customer verification conducted when the money laundering risk, fraud, or terrorist financing is greater. EDD detects early red flags for medium-risk customers while being a risk-based measure. EDD is vital in regulatory compliance against AML laws and avoids reputational as well as financial loss. EDD makes the financial institution aware of the customer’s background, origin of funds, and intention of transactions.

EDD vs Standard Due Diligence

- Scope: EDD is deeper than SDD, which only confirms rudimentary identity and business information.

- Risk Level: SDD is utilized for low-risk customers, and EDD for medium and high-risk profiles.

- Monitoring: EDD entails ongoing and anticipatory monitoring; SDD generally involves interval checks.

- Documentation: EDD needs more documentation and validation than SDD.

- Approval Process: EDD tends to involve escalation to compliance teams or higher management, in contrast to SDD.

Regulatory Compliance

- KYC (Know Your Customer) regulations are mandated to prevent money laundering, fraud, and financing of terrorism.

- In India, the Prevention of Money Laundering Act (PMLA), 2002, regulates KYC guidelines for financial institutions.

- Reserve Bank of India (RBI) releases KYC Master Directions, which mandate how customer identification and verification are to be carried out.

- Periodic updation or re-KYC is needed to maintain customer information up to date, depending on the risk profile of the customer..

Conclusion

Medium-risk customer Re-KYC is an essential component of regulation adherence and effective risk management. Given the dynamic evolution of financial regulations, customer details must be periodically updated in the records by institutions to ensure correctness, detect fraud, and build trust. Effectively executed Re-KYC practices with sound and secure methodologies contribute not only to organizations staying in compliance but also to enhancing operational effectiveness and customer satisfaction.

Our identity verification API simplifies and automates the Re-KYC process of medium-risk consumers. With verification of real-time data, safe document check, and smooth integration functionality, it helps financial organizations meet regulatory timing without compromising ease of use by customers.

FAQ

Who is considered a medium-risk customer?

Medium-risk customers generally possess moderate levels of transaction volume or profiles indicating a balanced degree of risk, neither too low nor too high.

Why is Re-KYC important?

It assists financial organizations in identifying unusual behavior, avert fraud, and provide proper records as per compliance rules.

What are the documents required for Re-KYC?

Typically, identity and address proof updated documents are sought. Certain institutions might also seek a recent photograph or additional affirmations.

Is digital Re-KYC possible?

Yes, institutions increasingly provide digital Re-KYC through mobile apps or online platforms, employing technologies such as video KYC or Aadhaar-based authentication.

How does your identity verification API assist in Re-KYC?

Our API facilitates fast, automated KYC verification by checking IDs, extracting information, and enabling real-time document uploads.