Regulatory compliance has become the pillar of businesses, especially for Payment Service Providers (PSPs). Identification and verification of Ultimate Beneficial Owners (UBOs) is one of the key areas of compliance. As financial crimes like money laundering and financing of terrorism evolve to be more sophisticated, regulators around the globe are making stricter requirements to procure transparency in the ownership structures.

With enhanced oversight from regulators and enhanced complexity of international financial networks, PSPs face the pressure of putting in place strong due diligence processes. Misidentification and non-verification of UBOs can lead to significant fines, reputational harm, and business interruption. This blog explores what UBO compliance is, why PSPs need to care particularly, and how providers can successfully navigate regulations.

Understanding Ultimate Beneficial Ownership (UBO)

Ultimate Beneficial Ownership (UBO) is the final owner or controllers of a legal entity or business company even when the ownership might be through successive companies or arrangements of a legal nature. Identifying the UBOs is important in avoiding the concealment of legal persons for use with illegal objectives, and achieving the transparency in finance transactions. Through complex structures within companies, owners tend to go unnoticed; due to this fact, discovering real ownership requires the investigation of effective ownership.

UBO identification is critical in the financial sector for anti-money laundering (AML) and counter-terrorism financing (CTF) purposes. Financial institutions have a legal obligation to conduct due diligence and determine UBOs at onboarding and during the business relationship. Not identifying UBOs leaves businesses vulnerable to legal, financial, and reputational risks such as fines and sanctions. Global regulatory authorities such as FATF, EU, and FinCEN have established guidelines and requirements for UBO identification and reporting.

Controlling ownership interest’ means holding in excess of 10% of the shareholding, capital, or profit share of a company, states RBI.

Regulatory Framework for UBO Compliance

FATF Guidelines

- Financial Action Task Force (FATF) provides international standards on counter-terrorism financing (CTF) and anti-money laundering (AML)

- FATF advises identifying and validating the UBO of legal persons and structures.

- Jurisdictions should have precise and current UBO information and make it available to capable authorities.

UBO Compliance and its Effect on Financial Institutions

- Financial institutions are required to carry out enhanced due diligence (EDD) to identify UBOs under Know Your Customer (KYC) requirements.

- Institutions are required to collect and verify information regarding UBO, and to report any suspicious activity.

- Compliance reduces the risk of being exposed to financial crimes and enhances the reputation of the institution.

Consequences of Non-Compliance

- Non-compliance can result in heavy fines by regulatory authorities, sanctioning the business and/or licensing suspension, and fines under the law.

- Your institution would lose its reputation and opportunity to conduct business.

- Continued or willful failure to comply would lead to criminal charges against individuals and entities involved.

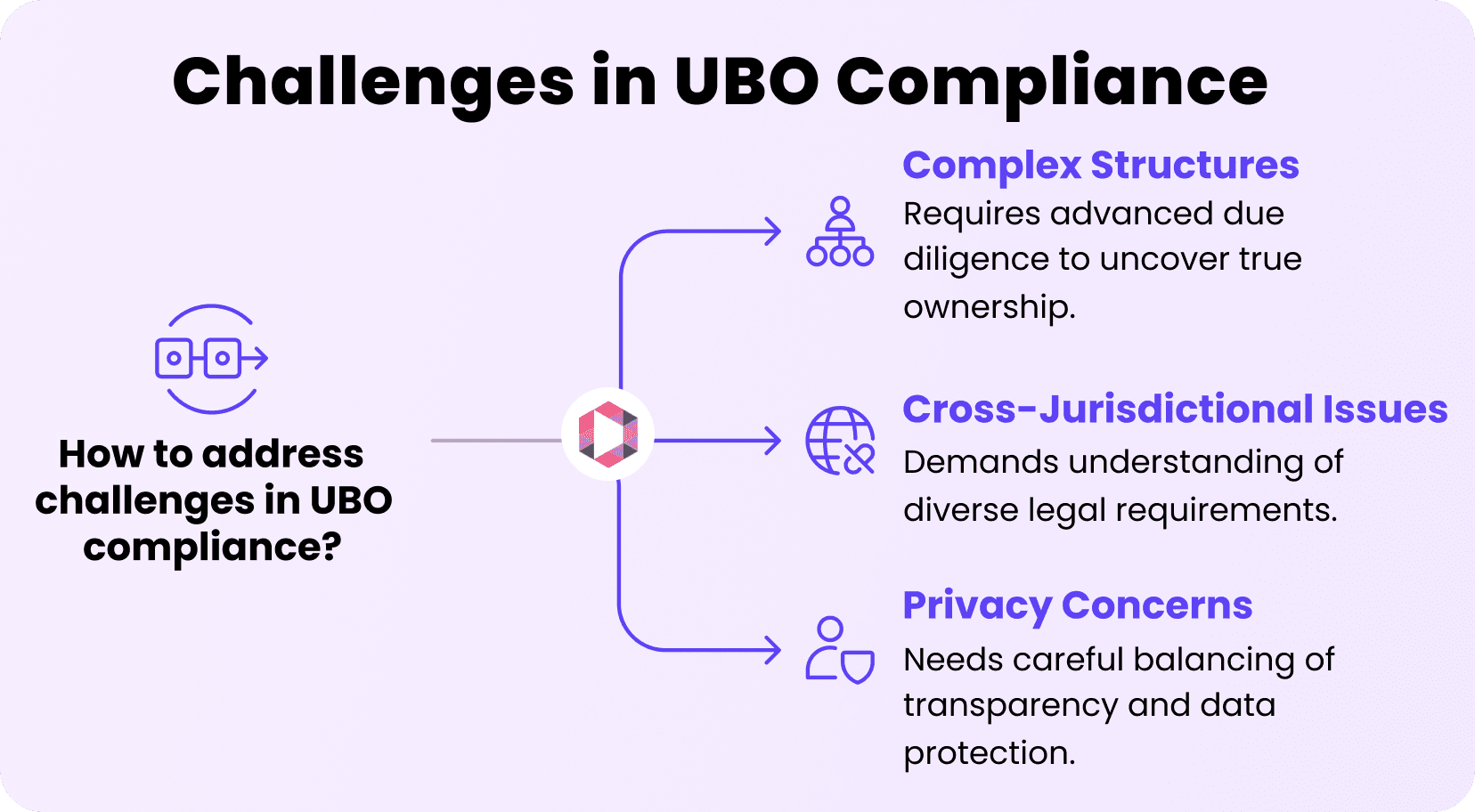

Challenges in UBO Compliance

- Complex Corporate Structures: Determining the true beneficial owner becomes difficult when multiple layers of ownership exist, and ownership is obscured by the use of shell companies or trusts in the ownership structure.

- Cross-Jurisdictional Issues: Complying with UBO requirement can prove to be complicated when entities are registered in more than one country with different legal definitions and disclosures requirements, and transparency levels.

- Privacy Concerns: It can be hard to find a balance of transparency while also complying with data protection laws and not disclosing UBO information that privacy laws may protect in some jurisdictions.

Benefits of UBO Compliance for Payment Service Providers

- UBO compliance helps payment service providers identify and avoid money laundering, fraud, and other financial crimes, reducing overall financial risk.

- By verifying the actual identities behind commercial entities, vendors can have transparency and impose more stringent standards of due diligence on their operations.

- Exhibiting high compliance commitment increases the credibility of the provider with regulators, partners, and customers and facilitates deeper business relationships.

- Maintaining compliance with UBO regulations averts significant fines, legal proceedings, and regulatory penalties, leading to smooth and continuous business processes.

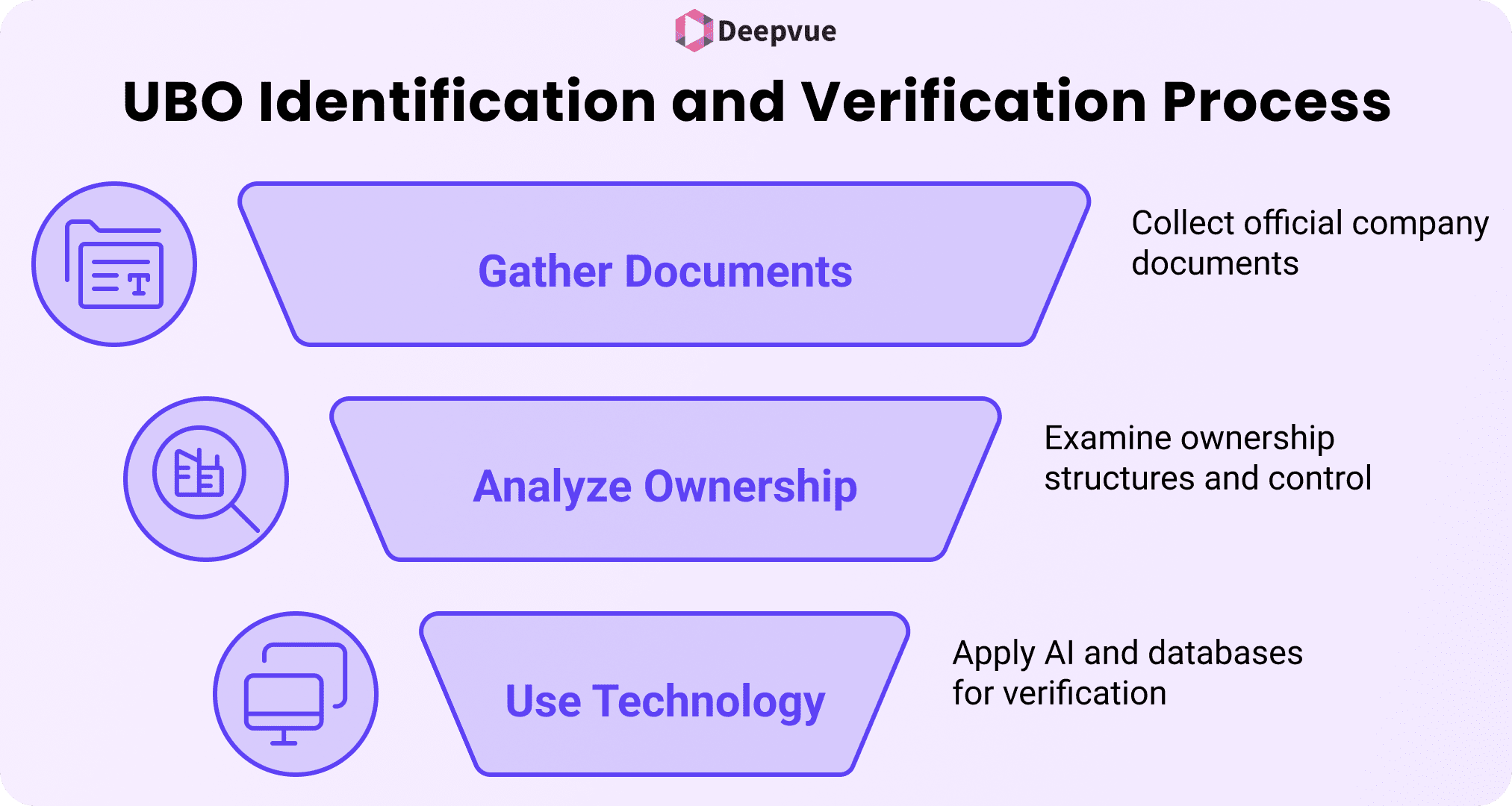

Processes for UBO Identification and Verification

- Gathering and Scrutinizing Company Information: Obtain official documents like incorporation certificates, shareholder registers, and company bylaws. Examine the legal structure, business activities, and registered addresses of the entity.

- Analyzing Ownership Structures: Identify those who directly or indirectly own (commonly 25% or more) or control. Examine complex or layered ownership arrangements to trace the chain of ownership. Consider individuals with significant influence or decision-making power, even if they lack direct ownership.

- Utilizing Advanced Technologies: Use automated tools and databases to cross-reference company and shareholder information. Use AI and analytics to identify hidden ownership, shell companies, or unusual patterns. Use e-KYC platforms, document verification APIs, and beneficial ownership registries for precision and compliance.

Future Trends in UBO Compliance

Governments and international bodies are tightening regulations around UBO disclosure to combat money laundering, tax evasion, and terrorism financing. Additional countries are establishing centralized UBO registries and requiring tighter reporting obligations for legal persons. Regulators such as the FATF (Financial Action Task Force) are driving increased transparency and international cooperation.

Sophisticated technologies like AI and machine learning are being applied to compliance systems to improve risk detection and due diligence processes. Blockchain is becoming a secure and transparent platform for recording and verifying UBO data. RegTech solutions are automating UBO verification, continuous monitoring, and reporting, minimizing human errors, and enhancing efficiency. APIs and integrated platforms are facilitating real-time data sharing and quicker compliance processes across institutions.

Conclusion

As regulatory requirements continue to tighten, Ultimate Beneficial Owner (UBO) compliance has become unavoidable for Payment Service Providers. Accurate identification and verification of UBOs is not merely a matter of legal compliance—it’s about promoting transparency, avoiding financial crime, and ensuring the integrity of the payments ecosystem. For PSPs, being ahead is about investing in robust compliance infrastructures, utilizing technology for effective due diligence, and keeping up with changing global regulations. Prioritizing UBO compliance not only reduces risk but also earns payment service providers credibility with partners, clients, and regulators.

FAQs

What is an Ultimate Beneficial Owner (UBO)?

A UBO is the one who finally owns or controls an organization, though indirectly. He is the actual beneficiary behind an arrangement or a legal entity.

Why is UBO compliance important for Payment Service Providers (PSPs)?

UBO compliance protects PSPs against fraud, money laundering, and terrorist financing and ensures they are within the law and regulations.

Who is a UBO?

Generally, a UBO is an individual who holds 25% or more of a business entity or has control over it. This figure could differ from one jurisdiction to another.

Which are the primary regulations controlling UBO compliance?

UBO control is framed according to FATF recommendations, EU AML directives, and regional financial authority guidelines, as the area of operation would differ.

How do PSPs validate UBO details?

PSPs conduct Know Your Customer (KYC) verification, ask for formal documents, and employ third-party databases or utilities to confirm ownership arrangements.